Related Articles

After many research trips to Japan, we moved to increase some of our exposure to businesses supported by key trends, such as digitalization and advanced computing, industrial innovation, unique consumer preferences, and an aging domestic and global population.

Key Points

- Japan is experiencing a resurgence, driven by demand for its industrial automation brands, corporate governance reforms, and a reenergized consumer class.

- Macroeconomic factors such as wage growth, inflation normalization, and global supply chain shifts, and Japan’s neutrality and proximity to the rest of Asia, can create a favorable backdrop for investment.

- We’ve found opportunities investing in some of the country’s most innovative companies that are blending tradition with cutting-edge technology to redefine their industries and expand across geographies.

In 1908, Kikunae Ikeda, a Japanese scientist, sat down for a simple meal of kombu dashi, a broth made from seaweed. As he sipped, he noticed something extraordinary. The taste was unlike the standard categories of sweet, sour, salty, or bitter. Determined to uncover the secret behind this unique flavor, Ikeda identified the compound responsible: glutamate, an amino acid, which would later be known as umami, the fifth taste.

Ikeda’s discovery led to the founding of Ajinomoto in 1909, a company built around bringing umami-rich seasonings to the world. But the story didn’t end with food. Over the past century, Ajinomoto has expanded into biotechnology, pharmaceuticals, and even semiconductor materials, applying its expertise in amino acids to industries far beyond its original vision. This ability to reinvent and innovate while staying true to its roots is emblematic of Japan’s broader transformation.

Today, Japan is experiencing a resurgence, driven by corporate governance reforms, automation, and a reenergized consumer class. While macroeconomic factors such as wage growth, inflation normalization, and global supply chain shifts can create a favorable investment environment, we believe the country’s real strength lies in its most innovative companies. Firms such as Ajinomoto are blending tradition with cutting-edge technology to redefine their industries and expand their operations to a global scale.

The Sun Rises

For years, Japan was dismissed by many global investors as a stagnant market. But macroeconomic and structural tailwinds are helping to change its image. It is too early to determine how tariffs and trade tensions will affect businesses with international operations. However, inflation and wage growth, after decades of stagnation, have reignited domestic consumption. Corporate governance reforms initiated by the Tokyo Stock Exchange are improving capital efficiency and transparency, with more companies returning cash to shareholders. A weakened yen has also enhanced export competitiveness, benefiting automation, high-end manufacturing, and consumer goods. While currency fluctuations can be volatile, Japan’s positioning in global supply chain shifts remains a long-term strength.

These macroeconomic and structural factors indeed support the investment case. However, our interest in Japan is rooted in bottom-up innovation and select companies that are reshaping industries ranging from semiconductor manufacturing to healthcare to precision food science.

Our goal is to identify companies with strong fundamentals, competitive advantages, and long-term growth potential that are supported by key secular trends. After many research trips to the country, we decided Japan was underrepresented in some of our portfolios and have increased our exposure accordingly to businesses supported by key trends, such as digitalization and advanced computing, industrial innovation, unique consumer preferences, and an aging domestic and global population. Many of the companies we own are leveraging one or more of these themes to build new business lines, often using early success as a springboard for broader expansion. This pattern of second and third acts has been demonstrated by the most successful companies in our portfolios. These businesses frequently surprise to the upside by entering adjacent markets or expanding geographically, enabling them to sustain elevated growth rates well beyond market expectations. In Japan, as in other markets, we have found selectivity is important as only a small number of businesses generate the bulk of returns.

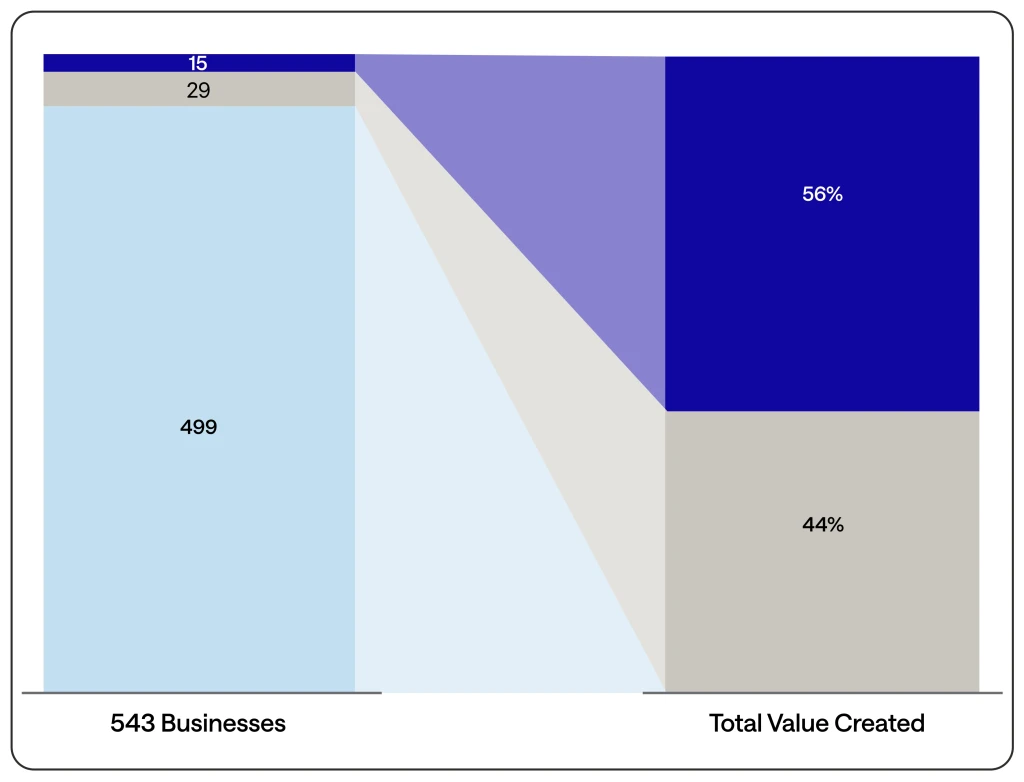

Exhibit 1

A SMALL NUMBER OF BUSINESSES GENERATE THE GREATEST WEALTH

Fifteen businesses created 56 percent of MSCI Japan Index total value

The Winds of Change

Digitalization and Advanced Computing

One of the most compelling secular trends in Japan is its role in enabling next-generation computing. While U.S. giants lead in chip design, Japan’s materials and component suppliers are essential enablers. Ajinomoto, for instance, has put its century-old amino acid expertise to use to build one of its most promising businesses; and a business that, in our view, is creating a long-term opportunity that is underappreciated by the market.

The company has created an unrivaled insulation material that is used in advanced semiconductor packaging. It is high value and low cost and mission critical to chip performance. We expect demand for this Ajinomoto Build-Up Film, or ABF, to accelerate exponentially as chip architectures grow more complex, especially in artificial intelligence (AI), high-performance computing (HPC), and server-class environments.

Ajinomoto not only benefits from more GPU (graphics processing unit)/AI server sales, but more importantly from the amount of ABF in each one. Complexity means more layers, more connectors, and more surface area, all of which need to be covered by ABF. We expect this demand to drive faster ABF sales, likely at higher prices. A business-profit margin of almost 20 percent for full-year 2025, compared with about 11 percent for the company overall should in turn help uplift overall margins for the company, leading to faster bottom-line growth.1

Together with Ajinomoto, HOYA, best known for its eyeglass lenses, anchors Japan’s increasingly critical role in enabling the infrastructure behind global digitalization. HOYA is the monopolistic supplier of extreme ultraviolet lithography mask blanks, which are vital for producing advanced AI chips, and also leads in high-precision glass substrates for hard disk drives. These technologies are central to the data proliferation underpinning AI, Internet of Things (IoT), and cloud computing.

As demand for high-performance chips intensifies globally, HOYA’s specialized components have become even more essential. R&D in precision optical technology for semiconductor lithography helps produce the microchips necessary for AI and other complex computing applications. Within its high-tech segment, we believe HOYA is well positioned to benefit from increasing semiconductor complexity and data proliferation.

Automation Nation

Japan has long been a pioneer in automation, but its relevance is increasing amid labor shortages, rising wages, and reshoring. Many of Japan’s businesses have transformed their product lines to meet growing demand for industrial automation products and services. This demand has become even more acute as the workforce shrinks, labor costs rise, supply chains shift, and the nature of work becomes more dangerous.

At the industry level, leaders such as Keyence and Advantest are extending Japan’s dominance in factory automation with intelligent sensors, control systems, and pneumatic technologies. These are all critical to building the “smart factories” of the future.

Founded in 1974, Keyence, which plays a key role in ensuring that components are assembled efficiently and cost-effectively, has been a beneficiary of this demand. The company is essentially unrivaled in bringing sensors to manufacturers and boasts clients across industries from aerospace to semiconductors. We believe that industrial automation will continue over the next decade and has demonstrated its merits during times of crisis and weak macroeconomic environments.

As manufacturing becomes more data-driven, the company’s high-end sensors and vision systems enable real-time process monitoring and quality control, key components of the “smart factory.” By integrating AI and cloud-based solutions, Keyence stands at the cutting edge of complex computing in industrial environments.

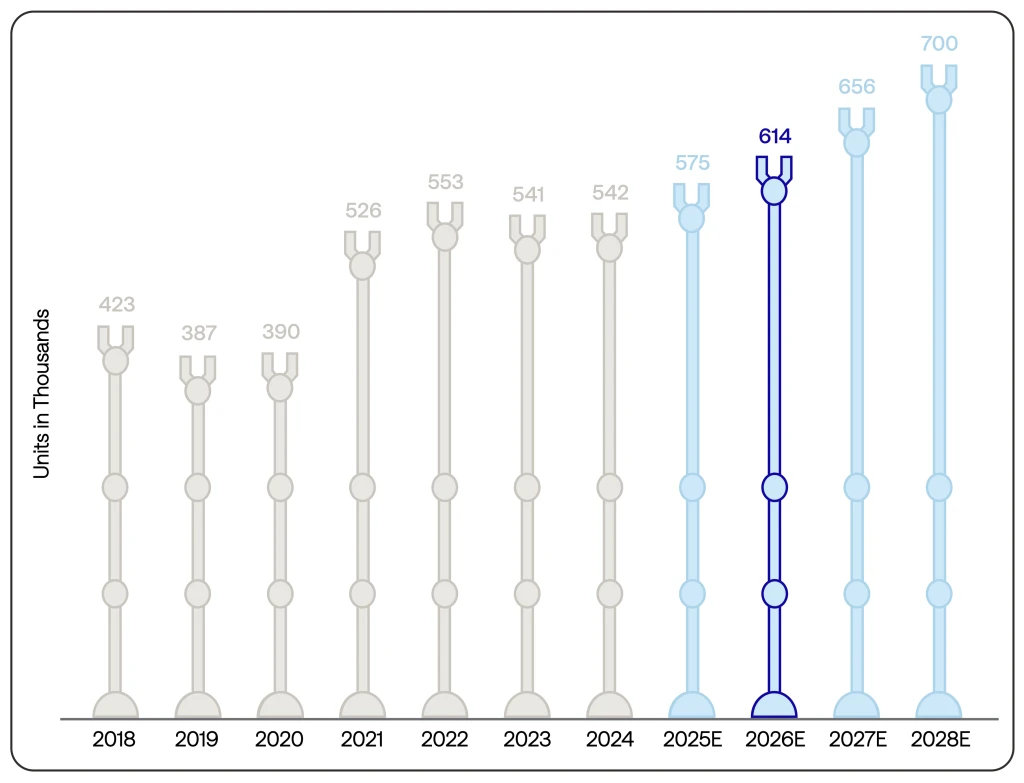

Exhibit 2

Global Demand for Automation Could Drive Demand for Intelligent Parts

Annual Installations of Industrial Robots: 2018 to 2024 and 2025 to 2028

Advantest plays a similarly important role in the semiconductor industry. The company is a leading supplier of automated test equipment, which determines whether chips operate properly and meet demanding performance and durability requirements. As semiconductors become larger and more complex, particularly in GPUs, custom chips, and high-bandwidth memory, testing has become more critical, more time-intensive, and more technically demanding.

This creates a growth opportunity for Advantest. More chips, longer test times per chip, and higher quality assurance requirements are increasing demand for its systems. The company’s tools are already deeply embedded in customer workflows, making switching costly and risky. In our view, Advantest is well positioned to benefit from the rising complexity of advanced semiconductors and the continued automation of quality control across the chip supply chain.

Automation solutions have become cheaper and more effective over the past five years. More industries are starting to see value in deploying them. We see increased demand in consumer electronics, food and beverage, pharmaceuticals, medical devices, furniture manufacturing, and even toy production. And we expect that demand for automation will be persistent, growing at about a 10 percent compound annual growth rate for the next decade or so.2

Unique Consumer Preferences: Quality, Novelty, and the Globalization of Taste

Japan’s consumers are among the most sophisticated in the world. They demand quality, value, and innovation. Their preferences are shaped by cultural refinement, a deep awareness of health and wellness, and a strong sensitivity to brand and experience. As wage growth returns and deflationary expectations fade, this consumer base is reawakening. And many companies that understand it are thriving both at home and abroad.

Ajinomoto has long understood how to anticipate and respond to the nuances of Japanese consumer behavior. While its MSG (monosodium glutamate) legacy may define public perception, the modern Ajinomoto is a leader in health-optimized food science. It has engineered a diverse portfolio of seasonings, ready-made meals, and nutrition-forward products, many of which are lower in sodium and fat and enriched with functional benefits. The company also introduced its Food-as-a-Service platform in Japan. This comprehensive model combines diagnostics, personalized dietary planning, and food delivery. It is designed especially for aging and health-conscious consumers.

At the same time, Ajinomoto has expanded internationally, adapting its offerings to the tastes and dietary norms of local markets across Southeast Asia and Latin America. With over 70 percent of its food and seasoning sales now generated overseas, the company has built a model of “glocal” relevance, combining Japanese innovation with local authenticity. Its value ladder strategy, where consumers in emerging markets begin with basic umami and move up to more premium menu-specific solutions, is designed to capture income growth and dietary sophistication as middle classes expand.

Whereas Ajinomoto exemplifies scientific precision and a wellness-forward evolution, Pan Pacific, operator of the Don Quijote retail chain, embodies Japan’s retail theater: an immersive, eclectic, and convenience-driven consumer experience that has developed into a cultural phenomenon.

Don Quijote, or “Donki” as it’s affectionately known, is more than a discount store. It is a high-density maze of sensory stimulation, offering everything from groceries and household staples to luxury handbags and novelty gadgets. Many of its stores are open 24/7. Aisles are packed, signage is loud, and every square inch is used for merchandising. This format might seem chaotic, but it’s engineered to create discovery, surprise, and impulse, three things modern consumers increasingly value.

Don Quijote’s genius lies in its ability to blend high-frequency necessities with aspirational indulgences, all under one roof. And it has achieved this not just in Japan but across international markets, including Singapore, Thailand, and the United States, where it is exporting the uniquely Japanese “Donki” experience to global shoppers curious for quality and quirk.

The company is also capitalizing on Japan’s booming inbound tourism sector. Stores cater explicitly to tourists, with multilingual signage, duty-free processing, and tailored product selections. Tourists come looking for souvenirs and stay for the spectacle. This retail model turns foot traffic into high-margin transactions while strengthening brand identity.

In essence, Ajinomoto and Pan Pacific reflect two sides of the same evolving consumer reality: one is clinically precise, health-optimized, and science-forward; the other is dynamic, experiential, and delightfully unpredictable. Both have succeeded by staying close to what Japanese (and increasingly global) consumers want: better quality, personalized experiences, and a sense of discovery.

Aging Populations: A Long-Term Demand Catalyst in Japan and Beyond

Japan is at the forefront of a demographic transformation reshaping many developed economies. With about 30 percent of its citizens now aged 65 or older, a figure expected to rise significantly in the coming decades, the country represents a striking case study of the challenges and opportunities associated with aging societies. Longer life expectancy, driven by advances in healthcare, improved nutrition, and rising living standards, is fundamentally altering the country’s social and economic fabric. While these shifts pose headwinds to headline GDP growth, such as labor shortages, pension burdens, and softer aggregate consumption, they are also driving increased demand for products and services that support safety, autonomy, and wellness in old age.

For long-term investors, the implications are twofold: aging societies may constrain traditional economic levers, but they also catalyze innovation in sectors such as elder care, medical technologies, functional food, infrastructure, and health-focused consumer goods. Companies such as Ajinomoto and HOYA have begun to align themselves with these secular trends, tailoring offerings to better serve senior consumers both in Japan and abroad. Ajinomoto, for instance, now uses its protein expertise to manufacture genetic medicines as well as functional food.

One of the most direct manifestations of this demographic shift is the increasing demand for accessible, reliable, and modernized urban infrastructure, elevators chief among them. More than 40 percent of elevators in Japan are now over 20 years old, and as a growing share of elderly residents live in multi-story apartment buildings, pressure is mounting on building owners to retrofit aging systems for barrier-free access, safety compliance, and energy efficiency. Japan Elevator Service (JES), the country’s largest independent elevator maintenance provider, is well positioned, in our view, to meet this long-term need. Unlike elevator manufacturers, JES services elevators across all major brands, offering building owners the ability to consolidate servicing under a single provider. Its offerings are deeply integrated with proprietary remote monitoring systems, predictive diagnostics, and a dense technician network that ensures high reliability and uptime. With a corporate philosophy of “Safety Above Anything Else,” JES has earned the trust of building managers and residents alike. This is an especially important differentiator in a market that prizes safety and reliability. With more than 120,000 maintenance contracts, high customer retention, and a growing modernization pipeline, JES has built a capital-light, cash-generative business model that stands to benefit directly from structural demographic trends.

Importantly, JES’s business is driven almost entirely by domestic structural demand, insulating it from many of the risks that face export-oriented or globally exposed Japanese companies. Its core services are delivered locally and tied to the predictable needs of Japan’s aging population and mature building stock, making it largely immune to fluctuations in tariffs, global trade, or geopolitical tensions. This profile aligns it with other demographic compounders, such as Ajinomoto and HOYA.

Ajinomoto is leveraging its deep amino acid research capabilities to develop functional food products that support muscle health, cognition, and longevity. These areas are of acute relevance in a country where sarcopenia and dementia are growing public health concerns. The company’s ability to deliver science-backed, palatable nutrition products has made it a leader in preventive healthcare consumption.

Meanwhile, HOYA is capitalizing on increased visual health needs among older populations while also capturing share in the growing global myopia market. Its dominant position in pediatric myopia lenses in China offers high-margin, recurring revenue that complements its domestic aging tailwind. Together, these businesses represent a broader investment theme: while Japan’s demographics pose macroeconomic headwinds, they also underpin durable, highly focused growth opportunities across safety, wellness, and essential services.

Japan’s Sogo Shosha: Global Gateways for Japanese Industry

While Japan’s sogo shosha may not align directly with the secular themes we have discussed, these general trading companies have long played a foundational role in shaping the nation’s economic landscape. Emerging in the postwar period, they were instrumental in rebuilding Japan’s industrial base and integrating domestic businesses into global supply chains. Today, they continue to serve as strategic enablers for Japanese industry, offering scale, reach, and operational breadth in an increasingly complex global economy.

Unlike traditional trading houses, sogo shosha are deeply embedded across value chains, functioning not only as intermediaries but also as owners, operators, and investors. Their expansive portfolios span energy, metals, chemicals, machinery, food, retail, and finance, providing diversified exposure to shifting global demand while helping mitigate risk.

Itochu is an example of the modern sogo shosha. Founded as a textile trader, the firm has transformed into a global conglomerate with eight core business divisions, from digital transformation and consumer retail to sustainable energy, many of the same themes we have already highlighted. Its stakeholder-oriented philosophy, creating value for sellers, buyers, and society, guides its operations and underscores its long-term resilience.

Among the major players, we believe it has demonstrated it is among the best stewards of capital, high-quality operators, with an attractive mix of portfolio businesses. Our conviction in Itochu is less about the individual businesses, and more about management’s strong track record, philosophy, and process around allocating capital to attractive businesses, and in improving the profitability of businesses it acquires, and divesting or exiting businesses that are or have become less attractive. Over the next seven years we expect Itochu’s total revenue to increase more than 50 percent.

As Japan modernizes its economic model, firms such as Itochu demonstrate how legacy institutions can continue to thrive while remaining grounded in tradition and bold in innovation.

Looking Ahead: Opportunity Amid Structural Shifts

Japan’s aging population is often viewed through a macroeconomic lens of potential risk. But as investors, we see it as a durable theme that can fuel demand for innovation, specialization, and recurring revenue. Companies such as Ajinomoto and HOYA demonstrate how thoughtful product development and long-range strategy can convert demographic pressure into opportunity.

More broadly, Japan itself is undergoing structural transformation. Global supply chain diversification is redirecting manufacturing to regions with geopolitical stability and deep technical expertise, two of Japan’s key strengths. The rebound in inbound tourism is not only restoring spending in key sectors but shifting consumer preferences toward experiences, wellness, and premium services. At the same time, Japan’s commitment to clean energy and decarbonization is spurring long-term investments in infrastructure, renewables, and next-generation technologies such as hydrogen and advanced nuclear.

We see these dynamics as reinforcing, not competing with, the opportunity set tied to aging demographics. Together, they paint a picture of an economy where innovation is not just encouraged but required. This environment is creating a new class of Japanese companies: globally competitive, technologically advanced, and socially relevant.

At Sands Capital, we are committed to identifying and investing in these companies, those whose innovation addresses society’s most pressing challenges and, in doing so, have the potential to create long-term wealth for our clients. As demographic, technological, and environmental forces converge, we believe the ability to navigate complexity and deliver impact will define the next generation of market leaders. Looking ahead, we will continue to pursue businesses that don’t just adapt to the future but help build it.

1. Ajinomoto reports segment profitability using business profit, not EBIT. Business-profit margin is calculated as business profit divided by sales. For full-year 2025, Ajinomoto’s Healthcare and Others segment, which includes Functional Materials, reported sales of ¥98.9 billion and business profit of ¥17.3 billion, implying a margin of almost 20 percent. Ajinomoto’s companywide margin on the same basis was approximately 11 percent, based on sales of ¥1.584 trillion and business profit of ¥181.1 billion. Source: Ajinomoto Co., Inc., Consolidated Financial Results for the Fiscal Year Ended March 31, 2026.

2. https://www.precedenceresearch.com/industrial-automation-market

Disclosures:

The views expressed are the opinion of Sands Capital and are not intended as a forecast, a guarantee of future results, investment recommendations, or an offer to buy or sell any securities. The views expressed were current as of the date indicated and are subject to change.

This material may contain forward-looking statements, which are subject to uncertainty and contingencies outside of Sands Capital’s control. Readers should not place undue reliance upon these forward-looking statements. There is no guarantee that Sands Capital will meet its stated goals. Past performance is not indicative of future results.

All investments are subject to market risk, including the possible loss of principal. The growth style of investing may become out of favor, which may result in periods of underperformance. The strategies are concentrated in a limited number of holdings. As a result, poor performance by a single large holding of a strategy would adversely affect its performance more than if the strategy were invested in a larger number of companies. International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional and economic developments. The strategies may experience losses as they are subject to equity securities risk, market and issuer risk, selection risk, growth style risk, concentration risk, currency exchange risk, foreign company risk, derivatives risk and other economic risks that may influence returns.

Differences in account size, timing of transactions, and market conditions prevailing at the time of investment may lead to different results, and clients may lose money. A company’s fundamentals or earnings growth is no guarantee that its share price will increase. Forward earnings and revenue projections are not predictors of stock price or investment performance, and do not represent past performance. Characteristics, sector (and regional, country, and industry, where applicable) exposure, and holdings information are subject to change and should not be considered as recommendations.

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. There is no assurance that any securities discussed will remain in the portfolio or that securities sold have not been repurchased. You should not assume that any investment is or will be profitable. A full list of public portfolio holdings, including their purchase dates, is available here.

As of May 12, 2026, Advantest, Ajinomoto, HOYA, Itochu, Japan Elevator Service, Keyence, and Pan Pacific/Don Quijote were held across Sands Capital strategies. The companies represent all Japanese holdings and were selected by the authors on an objective basis to illustrate the views expressed in the commentary.

Sands Capital refers to the combination of Sands Capital Management, LLC, Sands Capital Alternatives, LLC and Sands Capital Horizons, LLC. All three firms are registered investment advisers with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. The three registered investment advisers share certain personnel, office space, and other resources.

Information contained herein may be based on, or derived from, information provided by third parties. The accuracy of such information has not been independently verified and cannot be guaranteed. The information in this document speaks as of the date of this document or such earlier date as set out herein or as the context may require and may be subject to updating, completion, revision, and amendment. There will be no obligation to update any of the information or correct any inaccuracies contained herein.