Related Articles

Stay Up To Date

Something has gone wrong, check that all fields have been filled in correctly. If you have adblock, disable it.

The form was sent successfully

What Matters

The Point

AI adoption may be moving from experimentation to deployment faster than the infrastructure needed to support it can expand.

The Proof

Demand appears viral, enterprise penetration remains below 2 percent, and many critical suppliers operate in capacity-constrained markets with high barriers to entry.

The Result

We believe select businesses along the AI value chain may be positioned to convert rising demand and scarce supply into durable earnings growth over time.

The first wave of generative artificial intelligence (AI) changed how people interacted with software. It made advanced models accessible through a simple interface. Users could ask questions, generate content, summarize information, and write code.

The technology was powerful, but it still depended on human direction. It waited for instructions. It completed the task it was given. It did not take much initiative.

We believe the next stage may be more consequential.

In some ways, the market may be only months past the iPhone moment of 2007. The long-term opportunity is visible, but the full range of use cases, business models, and infrastructure requirements is still forming.

The early evidence suggests this cycle could be unusually powerful because those forces are developing at the same time.

Agentic AI is beginning to move AI from a tool into something closer to a digital worker. Instead of only responding to prompts, agents can execute workflows, make decisions within defined parameters, and report back on progress.

This matters because it could expand AI from individual tasks into broader business processes. It could also make the technology more useful for enterprises, where the biggest productivity gains often come from connecting many steps across complex systems.

AI is not simply another software cycle. It may be a technology cycle in which usage can spread across people, companies, and eventually agents themselves at an unprecedented pace.

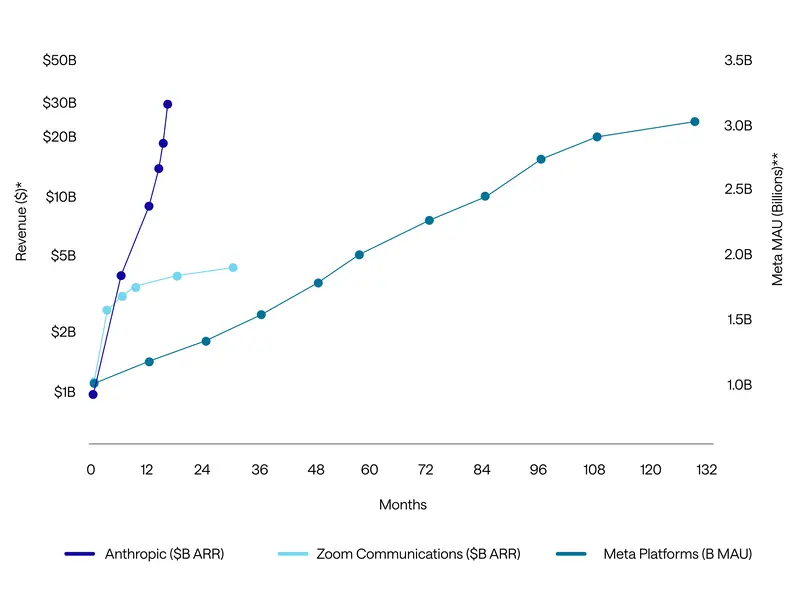

AI Demand Is Viral

Some technologies grow in a straight line. Others spread through network effects.

We believe AI belongs in the second group. Anthropic’s reported revenue trajectory, from roughly $1 billion to more than $47 billion in annualized revenue within about 12 months, points to a demand curve that is difficult to capture on a normal chart.

AI ADOPTION APPEARS TO BE SPREADING RAPIDLY

The technology is spreading through word of mouth, shared use cases, and visible productivity gains. One employee uses a model to save time. A colleague sees the output and tries it. A team turns a simple task into a repeatable workflow. A company then begins to ask where else the technology can be applied.

That pattern resembles earlier viral technologies. Zoom Communications spread rapidly during the pandemic because each meeting invited more users into the product. Meta Platforms scaled as more people joined social networks and made the platforms more useful to others.

AI may add another layer to that pattern. Human adoption can be viral, but agentic adoption could become even more networked. If agents begin communicating with other agents, executing workflows, and initiating tasks across systems, demand may grow through machine-to-machine activity as well as human use. That could make the adoption curve much steeper than investors expect.

This is the first reason the opportunity matters. Historically, periods of rapid technology adoption have often created significant investment opportunities, particularly when accompanied by disciplined attention to business quality and valuation.

AI is not simply another software cycle. It may be a technology cycle in which usage can spread across people, companies, and eventually agents themselves at an unprecedented pace.

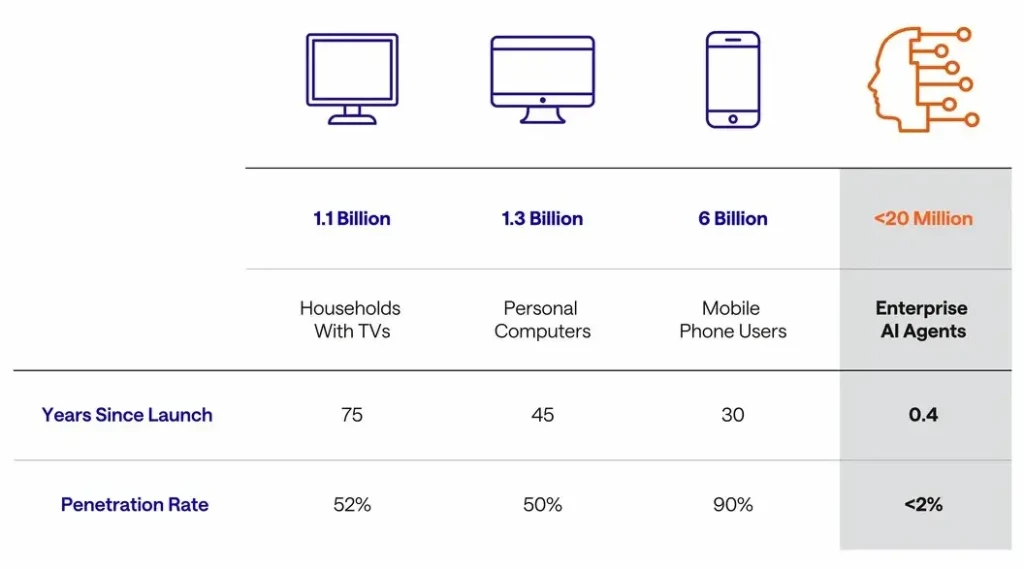

Enterprise Adoption Is Still in Its Infancy

The second condition is just as important. Consumer awareness of AI has grown quickly, but enterprise deployment is still at its infancy. Penetration rates appear to remain in the low single digits among global knowledge workers and is still concentrated in early use cases, especially coding.

Many companies are testing models, building pilots, and identifying use cases. Far fewer have embedded AI agents across core workflows at scale.

History offers useful context. Televisions, personal computers, and mobile phones took decades to reach broad penetration. Enterprise AI agents are only months into their adoption curve.

ENTERPRISE AI ADOPTION IS IN ITS INFANCY

That gap matters. The world has already invested heavily in AI infrastructure to support a very small installed base of agents. If enterprise adoption rises meaningfully from here, demand for the underlying infrastructure could be far larger than current levels imply.

We believe the analogy is simple. When the iPhone launched, the long-term opportunity did not require perfect foresight into every app or use case. It required recognizing that billions of people could eventually carry a powerful connected computer in their pocket.

AI may follow a similar logic in the enterprise. We do not need to know every future workflow to see that many knowledge workers and business processes could eventually use AI agents.

Over time, it is not unreasonable to expect penetration to move toward the vast majority of knowledge workers as models improve, costs fall, and enterprise systems become more deeply integrated.

This does not mean adoption will be smooth. Enterprises need security, reliability, compliance, integration, and clear returns on investment. They move more slowly than consumers. But slow early adoption can coexist with large long-term potential, especially when the technology keeps improving and the use cases keep expanding.

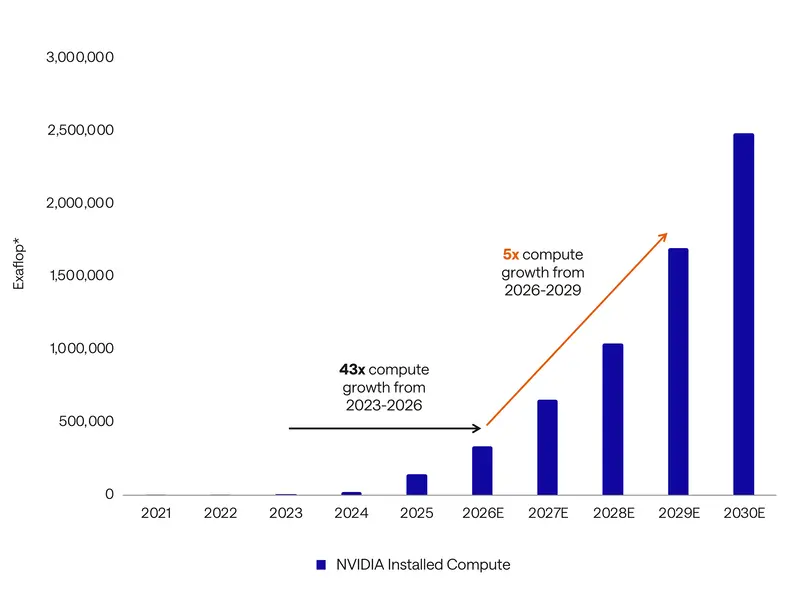

Supply Remains the Bottleneck

The industry has already installed a dramatic amount of additional compute to support today’s early AI adoption. Yet penetration remains low. That creates a basic tension. If adoption rates are still within single digits after a large increase in compute, what level of infrastructure will be needed at 10 percent, 25 percent, or higher?

Semiconductors sit at the center of that question. AI requires advanced logic chips, foundry capacity, high-bandwidth memory, networking equipment, power systems, and data center infrastructure.

These supply chains are complex, capital intensive, and difficult to expand quickly. Many of the key suppliers also operate in consolidated markets, where leadership positions, technical barriers, and limited capacity can support meaningful pricing power.

Even if the industry continues to invest, capacity may not grow fast enough to meet demand if enterprise adoption accelerates.

SEMICONDUCTOR CAPACITY MAY REMAIN A KEY CONSTRAINT

This is why we believe the semiconductor opportunity may remain larger and more durable than the market appreciates. The key issue is not only near-term chip demand.

It is the possibility that the entire AI infrastructure stack becomes a bottleneck for the next phase of digital growth for many years ahead. When viral demand, low penetration, and constrained supply appear together, we believe the setup can support multiyear value creation.

Memory could remain increasingly important as agents become more capable. Agents need to store, retrieve, and use information across tasks. Networking could become more important as models and workloads scale across data centers. Electricity could become more important as AI workloads make the economy more power intensive. Foundry capacity and semiconductor capital equipment could remain critical because advanced chips are difficult to manufacture, and capacity takes time to build. And of course, advanced AI chips themselves remain a key component.

Scarcity can create attractive growth, but it also creates risk. Capacity can eventually catch up with demand. Customers can optimize usage. New architectures can reduce cost. Valuations can move ahead of fundamentals. A disciplined approach must distinguish between temporary shortages and durable bottlenecks.

A Layered Opportunity

The AI opportunity will not stay in one place.

Early value has accrued to enablers because demand for chips, cloud capacity, power, memory, and data center infrastructure has grown faster than supply. These businesses remain critical bottlenecks, but infrastructure opportunities do not disappear simply because markets mature. Capacity expands. Costs fall. Competition shifts. But the infrastructure required to support a growing AI ecosystem may create more attractive investment prospects for years to come.

Over time, we also expect big value creation from the diffusion of AI in the economy. We name these AI businesses builders and beneficiaries. Builders will create new AI-powered products and services. Beneficiaries will use AI to strengthen existing businesses through better productivity, deeper customer engagement, or new sources of revenue.

This migration matters. In our view, it means AI should not be viewed only as a semiconductor cycle or a narrow technology trade. It is a broader change in how work is done, how products are built, and how companies compete and could persist for many years.

We believe select businesses along the AI value chain can create meaningful opportunities for long-term wealth creation. To us, this moment feels less like a mature technology cycle and more like the moment after Steve Jobs introduced the first iPhone. The platform had arrived, but many of the most valuable applications, businesses, and beneficiaries were still years away from emerging. We believe AI may be at a similarly early stage today.

The key will be identifying companies that can turn rising demand, scarce supply, and expanding use cases into durable earnings growth over time.

Disclosures:

The views expressed are the opinion of Sands Capital and are not intended as a forecast, a guarantee of future results, investment recommendations or an offer to buy or sell any securities. The views expressed were current as of the date indicated and are subject to change.

This material may contain forward-looking statements, which are subject to uncertainty and contingencies outside of Sands Capital’s control. Readers should not place undue reliance upon these forward-looking statements. There is no guarantee that Sands Capital will meet its stated goals. Past performance is not indicative of future results.

All investments are subject to market risk, including the possible loss of principal. Recent tariff announcements may add to this risk, creating additional economic uncertainty and potentially affecting the value of certain investments. Tariffs can impact various sectors differently, leading to changes in market dynamics and investment performance.

As of June 4, 2026, Anthropic, Meta Platforms, and NVIDIA were held across Sands Capital strategies. The companies identified represent a subset of current holdings and were selected by the author on an objective basis to illustrate the views expressed in the commentary.

Any holdings outside of the portfolio that were mentioned are for illustrative purposes only.

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. There is no assurance that any securities discussed will remain in the portfolio or that securities sold have not been repurchased. You should not assume that any investment is or will be profitable.

References to the “firm”, “we” or “our” are references to Sands Capital. Sands Capital refers to the combination of Sands Capital Management, LLC, Sands Capital Alternatives, LLC and Sands Capital Horizons, LLC. All three firms are registered investment advisers with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. The three registered investment advisers share certain personnel, office space, and other resources.

This communication is for informational purposes only and does not constitute an offer, invitation, or recommendation to buy, sell, subscribe for, or issue any securities. The material is based on information that we consider correct, and any estimates, opinions, conclusions, or recommendations contained in this communication are reasonably held or made at the time of compilation. However, no warranty is made as to the accuracy or reliability of any estimates, opinions, conclusions, or recommendations. It should not be construed as investment, legal, or tax advice and may not be reproduced or distributed to any person.