Road to the Future

Today, we view electrification, or the shift from vehicles with internal combustion engines to those powered by batteries, as one of the most important secular trends of the next decade.

Contributors

April 2023

Today, the future of the automotive industry seems clear. All vehicles are expected to eventually be connected to the world around them, capable of driving themselves, and powered by electricity generated mainly by alternative energy. However, it is taking time for these transitions to be realized.

For years, many of us have dreamed about what future transportation systems would look like. Some of our imagining was spurred by the futuristic cartoons of our youth. In 1962, Hanna-Barbera Productions added images to our dreams when it released The Jetsons. This whimsical family of the future darted about in aerocars, employed robots for housekeeping, and lived in Skypad Apartments, which was equipped with automated appliances.

While artificial intelligence (AI) has helped achieve smarter homes, advances in mobility have not kept pace with those in the Jetsons’ hometown of Orbit City. Over the past couple of years, however, the stars seem to have aligned for the electric vehicle (EV) industry, whose sales doubled in 2021 from the previous year. In 2012, 120,000 EVs were sold worldwide. In 2022 more than that were sold each week. Still, only 14 percent of global car sales were electric in 2022, creating an enormous runway for growth for automakers and their suppliers that are able to take advantage of this trend.[1]

How will these companies make the transition to a Jetsons-like world?

Ernest Hemingway perhaps said it best when writing about a man’s plunge into bankruptcy. It happens “gradually, and then suddenly.”

Gradually, Then Suddenly

As investors in innovative growth companies that are disrupting the status quo and attempting to create the future, we need to prepare for the day when gradually turns into suddenly. We have seen it happen myriad times throughout the past 100 years. It’s a bit of a variation on Moore’s Law, in fact. In the 90s, some people had cellphones. Today, we can’t live without them. The same pattern repeated with the internet, cloud computing, online shopping, and food delivery, and we are now seeing it in the growing adoption of EVs. We believe the ability to recognize the inflection point between nice-to-have and must-have is critical in building portfolios that will enable long-term wealth creation for our clients.

For EVs, the tipping point came when advances in technology, combined with demands for greater safety and reduced pollution, essentially forced automakers to enter the electric age. Consumers, who have grown increasingly aware of the negative climate effects of carbon emissions, have also become more enthusiastic about a more modern and greener approach to transportation. At the same time, parts makers have addressed some of the challenges causing adoption angst around EVs: driving range, battery safety, and availability of charging infrastructure.

Today, we view electrification, the process of replacing technologies that use fossil fuels with those that use electricity as their source of energy, as one of the most important secular trends of the next decade. In fact, we expect that 40 percent of new cars produced globally will be electric by 2030 versus about 14 percent in 2022. China, the European Union, and the United States are expected to lead this growth.[2]

Source: Electrek

This disruptive transformation has spurred a race for innovative technologies that make cars increasingly environmentally friendly, safe, and connected. That shift, which is basically substituting electricity for gasoline and oil, is already producing myriad opportunities for potential wealth creation by select businesses that are taking part in this transportation revolution.

Drivers, Start Your Engines

As long-term investors in innovative growth companies, we are well aware of the important role that Elon Musk and Tesla have played in advancing the vision for the EV industry and making consumers believe such a transformation was possible. Automakers around the world now scramble to keep up with Tesla’s avant-garde approach to transportation.[3]

We are excited about the opportunities that increased demand for EVs is creating for automakers and believe that a select number of them will capture a disproportionate share of industry profits. As the industry evolves, we continue to explore new spaces across the EV supply chain to identify businesses that could become critical enablers that support the success of EV manufacturers but do not assume the risk of choosing a winner in the field.

This is especially important because, while we feel certain that electrification and automation of transportation will happen, we cannot predict what vehicles will look like and do over the next 20 to 30 years. We do know that the components of these vehicles will need to be produced in state-of-the-art factories that are made more efficient by automation. We know that they will need batteries and parts that are used in battery production. Vehicles will need to be supported by smart architecture complete with automated driving and entertainment functions. And AI will be necessary to run the automated controls, safety features, and smart consoles that riders of the future will demand. Semiconductors, already indispensable in auto production, will be needed at every step of the way to ensure tomorrow’s vehicles become smarter and more powerful to handle the demands of their riders.

Supply-chain Economics

Some of the most often cited challenges to EV adoption include price, limited driving range, battery issues, and the availability of charging infrastructure.

We believe that businesses that are providing the parts and services that address these challenges by helping to automate factories, produce cheaper and better batteries, create sensors that power safety features, or design smart controls that will support a new driver experience should reap the benefits of the electrification trend. We expect these companies comprising the EV supply chain will have greater pricing power and growth potential than the industry as a whole.

As the appetite for EVs grows, so does the demand for the batteries, smart architecture, and artificial intelligence solutions that power the ride and provide the EVs’ automated safety, navigation, and entertainment features. Fully autonomous cars—those that respond to voice commands and not a steering wheel—may be decades away. However, automation is alive and well in manufacturing and in various systems that power an EV.

Assembly 3.0

Before even delving into the components and systems needed to make the vehicle of the future, we need to think about how these pieces will be put together most efficiently and cost-effectively.

While the auto industry is already one of the more automated industries, we believe the production of EVs will need to become increasingly complex to manipulate the volatile and dangerous materials needed to create the batteries. To handle these demands, factories will require increasing amounts of machine vision and precise measurement systems. We believe that Keyence is a leading provider of these solutions for the battery, motor, and inverters, and it benefits from its close relationship with automobile manufacturers and suppliers. We believe its well-established position should enable it to benefit from growth in the EV market and increase its market share.

Under the Hood

As part of our research into the EV supply chain, we seek to identify which component manufacturers are most critical to the supply chain, have significant competitive advantages, and will be most able to keep pace with the rapidly evolving EV industry.

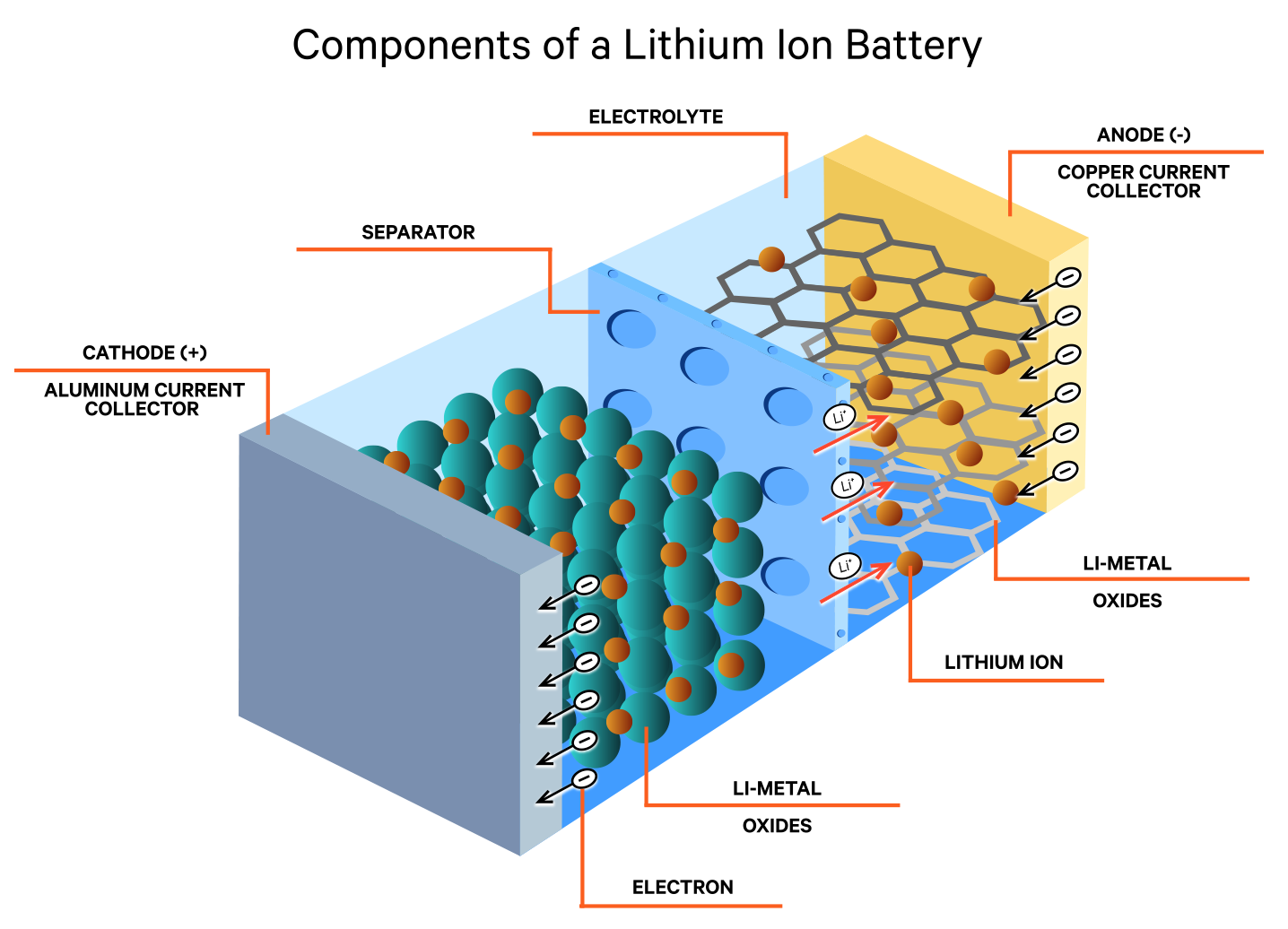

Batteries offer a key source of differentiation to automakers as competition among EV makers heats up. A battery is a critical determinant of driving ranges, recharging speed, and safety, which are all key sources of adoption angst in the mass-to-premium vehicle market and will be key contributors to the success of EV models.

While other EV batteries exist, lithium-ion batteries are most commonly used. Their cell units, cathodes, and anodes generate electric currents; electrolytes provide a safe and efficient channel for transmitting electricity; and separators prevent short circuiting and overheating. Over the next five to 10 years, we see opportunities for makers of lithium-ion battery components that will likely benefit as demand for EVs increases. We believe total demand for lithium batteries globally will grow at a 25 percent compound annual growth rate (CAGR) to 1500-plus gigawatt hours (GWh) by 2026 and 3000 plus GWh by 2030.[4]

We believe that battery makers, such as China’s Contemporary Amperex Technology (CATL) and South Korean Samsung SDI and LG Energy Solution (LGES), sit at a critical chokepoint of the EV supply chain.[5]

They function as intermediaries between the upstream raw material producers and battery components manufacturers and the downstream EV auto manufacturers and large-scale power and utility customers.

They have been able to build dominant market-share positions, thanks to their long operating track records, technological advantages, strategic relationships with original equipment manufacturers (OEMs) and across the supply chain, and scale. We believe these battery makers will benefit from this competitive advantage over the next five to eight years as well as their ability to offer cost-effective solutions to extend driving range, improve charging speed and recharging cycles, and minimize short circuits in the battery cell and accidental fires.

Consequently, the industry has consolidated. In 2021, the top five battery makers accounted for about 75 percent of battery cell output (in kilowatt-hours (kWh)), and we expect that percentage to increase over the next five to 10 years.[6]

Having conducted significant research into the components of the battery, we believe the most attractive opportunities within this space exist in the cathode and separator markets. We believe separator producers will achieve the highest average gross margins in the battery supply chain over the next five to seven years because no rare earth metals are required in separator production.

The cathode: Beyond the battery makers, we also see significant growth opportunities for manufacturers of key components in the battery cell, especially those focused on addressing the critical issues of driving range and battery safety. South Korea’s Ecopro BM is working on products to address range anxiety with its high-nickel cathodes for lithium-ion batteries, whose higher energy density can help increase the distance that a vehicle can drive on a charge.

We view high-nickel cathode (defined as NCM 811 or above) as disruptive technology due to its 25 percent higher energy density than mainstream NCM 622.[7]

High-nickel technology didn’t exist five years ago but now accounts for 11 percent of the overall cathode market. As demand for longer-range batteries grows, we believe the global average battery density of an EV will increase from the current 62 kWh to 80 kWh by 2025.

Ecopro BM currently controls about 35 percent of the high-nickel cathode market, supplying the battery makers. We expect the business will benefit from both growing EV battery demand and accelerated demand for its high-nickel cathodes. We expect demand for these cathodes to outpace demand for EVs, which should help Ecopro BM achieve a 50 percent CAGR in revenue over the next five years.[8]

Thanks to advances in its battery technology and its ability to aggressively expand capacity, the company has been able to gain share in a highly consolidated market.

The separator: Combating other challenges of EV adoption is SK IE Technology (SKIET). The business, headquartered in South Korea, has advanced the production of high-end (coated) wet battery separators that help prevent battery fires and improve battery safety. Separators, an essential component of any lithium-ion battery, are ultra-thin layers of polyethylene and polypropylene (PE/PP) that separate a battery’s cathode and anode, which prevents thermal runway, reduces fire risks, and improves battery life.

SKIET is the market-share leader in the high-end vehicle segment, supplying some of the world’s leading mainstream battery producers. Overall, we expect the separator market can sustain more durable growth rates because companies within this segment are able to maintain their pricing power because their products are harder to produce and replace. The design, prototyping, testing, and mass production of these separators take not only a stringent quality-control (QC) process but also years of time and the involvement of the vehicle manufacturer. The coating on SKIET’s separator is a key advantage because it makes the battery safer for longer by helping absorb heat that causes thermal runway, which can lead to battery fires. SKIET has a highly profitable business model and sticky long-term contracts with customers, which typically last between five and 10 years and, because of the QC process and significant time commitment, are difficult to switch out of.

Smart-vehicle architecture: The shift from internal combustion engines to electric and autonomous driving goes far beyond the battery and has begun to turn driving—once a practical task—into a curated user experience. This means increased demand for infotainment, digitalized and user-friendly access to such content, and increasingly autonomous capabilities. Ultimately, we will begin to interact with our cars more as we do with our tablets or televisions than with our current cars.

Aptiv, which already supplies computer technology to many of the world’s electrified vehicles, has been in the vanguard of driver-assisted technology for decades through its affiliations with General Motors and Delphi.[9]

Aptiv’s smart-vehicle framework is likened to a brain and nervous system of the car, with sensors serving as receptors to transmit messages to the vehicle’s central computer via satellite architecture. Many of Aptiv’s solutions are based on safety innovations and have been developed in line with its advanced driver-assistance systems (ADAS), including systems that enable autonomous vehicles.

We believe Aptiv is well positioned to benefit from the move toward automation and electrification as well as the increasing demand for greener solutions. Importantly, the company’s growth does not depend on increased auto production but rather on growing demand for its wide range of advanced global automotive technology that focuses on ADAS and connectivity software capabilities.

The automotive industry categorizes the levels of ADAS on a range of 1 to 5, with levels 1 and 2 providing safety backup—such as the autonomous emergency braking feature—to an engaged driver. Level 2 adds auto lane change, highway assist, and traffic jam assist, which allow drivers to take their hands off the wheel and their foot off the pedals. An example of level 3 functionality is the traffic jam “pilot,” which would essentially let the driver take their mind off driving in such a scenario. Levels 4 and 5 would layer on AI functions, including neural networks.

Levels of Driving Automation: The market currently supports the higher end of level 2 and the lower end of level 3 in terms of affordability, according to Aptiv, which calls this the sweet spot in which the benefit from these advanced safety systems can be maximized while minimizing the cost.

As cars become even more autonomous, we expect to see software that will create an increasingly digital experience.

Headquartered in China, Huizhou Desay SV Automotive plays a similar role but concentrates on serving China’s growing EV market. The company says it aims to seamlessly integrate man, machine, and lifestyle through its smart cabin, driving, and service solutions. Its cockpit of the future will include automation domain controller units that enable voice recognition, streaming media, digital displays of information about the car functions, surroundings, and front and back row karaoke integration, while the cameras, sensors and ADAS software will enable assisted parking, lane changing, etc. The company has a keen understanding of local cost advantages generated through its supplier relationship, and we believe it is well positioned to benefit from growth in China’s EV market as the country moves to localize its EV supply chain. Reports from 2021 suggest that smart cockpits are found in about 36 percent of cars . Over the next five years, we expect this number to grow to 60 percent in China, where the majority of Huizhou Desay SV Automotive’s business is based.[10]

The semiconductor: Semiconductors are another essential need in the EV supply chain. You cannot make a car without computer chips. The number and power of these chips will need to grow as vehicles become increasingly automated. To that end, a range of businesses in the semiconductor supply chain, including ASML, LAM, Taiwan Semiconductor, Texas Instruments, and Entegris, stand to benefit from the increased demand not only for more compute power but also for more complex compute power. Chipmaker NVIDIA, which provides AI and machine learning (ML) technology, has been working on an autonomous driving platform, which we believe could provide upside beyond its core AI/ML and gaming verticals. Notably, NVIDIA’s full stack driving platform features both one-time and recurring revenue streams, driven by its hardware and software components, respectively. We look at this company as a toll collector on a very long growth highway to vehicle automation. While our research indicates that AI/ML is early in its adoption, NVIDIA is encouraging adoption across industries and use cases by decreasing costs and simplifying implementation. Ultimately, we expect AI/ML applications to account for an increasing portion of EV input costs.

The Road to the Future

Looking to the future, we see opportunities among Chinese OEMs that have been able to establish leadership in technology, brand, and scale. We are especially interested in vertically integrated companies that not only produce cars but also make their own batteries, electric motors, and most of the components in-house. We believe this vertical integration could enable select companies to innovate and adopt new technologies faster. It would also allow lower production costs and selling prices that could have greater appeal to a mass market. We expect Chinese consumers will be among the fastest adopters of EVs because of government incentives for production and infrastructure that have given China a head start relative to other countries.

As visions of electrification collide with the prospects of AI, we expect not only to see increased ubiquity of EVs and their components but also an acceleration of the race for autonomous vehicles that we expect will dominate the longer-term mobility landscape.

Toward Autonomy

We expect that vehicles will become increasingly autonomous as regulations fall into place, consumer fears ease, and technology is further commercialized. We expect that automation will gain adherents in stages—autonomous features will be adopted faster than fully self-driving cars that no longer need a steering wheel or driver, which will get bogged down by regulation and consumer safety fears.

The rapid transformation of mobility inspires us all to look forward and to imagine a day—when like George Jetson—we can take to the air for our daily commute. As students of innovation, we will continue to explore possibilities that are changing not just the future of mobility but the future of the world. Our in-house research team continuously talks to leading thinkers, creators, and entrepreneurs who are exploring possibilities for smarter future mobility solutions, key hardware and software technologies, big data analytics, AI, and machine learning.

Our research into electrification sprang from our search to find businesses that were addressing alternative energy solutions in a world desperate to curb its carbon emissions. As we like to remind our investors and each other, sometimes it’s not about the destination but what we learn throughout our journey. Being able to draw insight from patterns of the past to anticipate the course of the future is how we aim to find exceptional businesses. Making these discoveries before the inflection point—when gradually becomes suddenly—is how we believe we can provide the exponential long-term wealth creation that we seek for our clients.

[1] Sands Capital research

[2] Source: Electrek

[3] Tesla is not owned in any Sands Capital strategy.

[4] Sands Capital research

[5] LGES is not held in any Sands Capital strategy.

[6] UBS analysis based on company data.

[7] Lithium nickel cobalt magnesium oxide

[8] Sands Capital research

[9] General Motors and Delphi are not held by any Sands Capital strategies.

[10] Sands Capital research based on Morgan Stanley 2021 data.

Disclosures:

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. There is no assurance that any securities discussed will remain in the portfolio or that securities sold have not been repurchased. You should not assume that any investment is or will be profitable. A full list of public portfolio holdings, including their purchase dates, is available here. A full list of private holdings is available upon request to qualified investors.

Unless otherwise noted, the companies identified represent a subset of current holdings in Sands Capital portfolios and were selected on an objective basis to illustrate examples of the range of companies involved in the production of EVs across public markets that have created new drivers of growth through the elective vehicles supply chain. They were selected to reflect holdings with varied business models across multiple geographies. This article is part of a larger series on digitalization and features businesses and related companies that were selected to illustrate current underlying macroeconomic and sectoral trends. The series uses rotation, whereby businesses featured, are selected to highlight different trends across sectors and geographies.

As of March 31, 2023, ASML was held in Global Growth, Technology Innovators, and International Growth. Aptiv was held in Global Growth, Global Leaders, International Growth, and Global Shariah.

CATL was held in Emerging Markets Growth. Ecopro BM, Huizhou Desay SV Automotive, and SK IE Technologies were held in Emerging Market Discovery. Entegris was held in Select Growth, Global Growth, and Global Leaders. Keyence was held in Global Growth, Global Leaders, and International Growth. LAM is held in Select Growth, Global Growth, Emerging Markets Growth, Emerging Markets ex China, Global Shariah and Technology Innovators. NVIDIA was held in Select Growth and Global Shariah. Texas Instruments was held in Global Leaders, International Growth, and Select Leaders. Taiwan Semiconductors was held in Emerging Markets Growth, Emerging Markets ex China Technology Innovators, International Growth, and Global Shariah. Tesla was not held in any Sands Capital strategy and is referenced for illustrative purposes only.

The views expressed are the opinion of Sands Capital and are not intended as a forecast, a guarantee of future results, investment recommendations, or an offer to buy or sell any securities. The views expressed were current as of the date indicated and are subject to change. This material may contain forward-looking statements, which are subject to uncertainty and contingencies outside of Sands Capital’s control. All investments are subject to market risk, including the possible loss of principal. Readers should not place undue reliance upon these forward-looking statements. There is no guarantee that Sands Capital will meet its stated goals. Past performance is not indicative of future results. A company’s fundamentals or earnings growth is no guarantee that its share price will increase. The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. There is no assurance that any securities discussed will remain in the portfolio or that securities sold have not been repurchased. You should not assume that any investment is or will be profitable. Company logos and website images are used for illustrative purposes only and were obtained directly from the company websites. Company logos and website images are trademarks or registered trademarks of their respective owners and use of a logo does not imply any connection between Sands Capital and the company. GIPS Reports found here.

References to “we,” “us,” “our,” and “Sands Capital” refer collectively to Sands Capital Management, LLC, which provides investment advisory services with respect to Sands Capital’s public market investment strategies, and Sands Capital Ventures, LLC, which provides investment advisory services with respect to Sands Capital’s private market investment strategies, which are available only to qualified investors. As the context requires, the term “Sands Capital” may refer to such entities individually or collectively.

As of October 1, 2021, Sands Capital was redefined to be the combination of Sands Capital Management, LLC and Sands Capital Ventures. Both firms are registered investment advisers with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. The two registered investment advisers are combined to be one firm and are doing business as Sands Capital. Sands Capital operates as a distinct business organization, retains discretion over the assets between the two registered investment advisers, and has autonomy over the total investment decision-making process.

Information contained herein may be based on, or derived from, information provided by third parties. The accuracy of such information has not been independently verified and cannot be guaranteed. The information in this document speaks as of the date of this document or such earlier date as set out herein or as the context may require and may be subject to updating, completion, revision, and amendment. There will be no obligation to update any of the information or correct any inaccuracies contained herein.

This material is for informational purposes only and does not constitute an offer, invitation, or recommendation to buy, sell, subscribe for, or issue any securities. The material is based on information that we consider correct, and any estimates, opinions, conclusions, or recommendations contained in this communication are reasonably held or made at the time of compilation. However, no warranty is made as to the accuracy or reliability of any estimates, opinions, conclusions, or recommendations. It should not be construed as investment, legal, or tax advice and may not be reproduced or distributed to any person.

In the United Kingdom, this communication is issued by Sands Capital Advisors – UK Ltd (“Sands UK”) and approved by Robert Quinn Advisory LLP, which is authorised and regulated by the UK Financial Conduct Authority (“FCA”). Sands UK is an Appointed Representative of Robert Quinn Advisory LLP. This material constitutes a financial promotion for the purposes of the Financial Services and Markets Act 2000 (the “Act”) and the handbook of rules and guidance issued from time to time by the FCA (the “FCA Rules”). This material is for information purposes only and does not constitute an offer to subscribe for or purchase of any financial instrument. Sands UK neither provides investment advice to, nor receives and transmits orders from, persons to whom this material is communicated, nor does it carry on any other activities with or for such persons that constitute “MiFID or equivalent third country business” for the purposes of the FCA Rules. All information provided is not warranted as to completeness or accuracy and is subject to change without notice. This communication and any investment or service to which this material may relate is exclusively intended for persons who are Professional Clients or Eligible Counterparties for the purposes of the FCA Rules and other persons should not act or rely on it. This communication is not intended for use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.