Related Articles

Stay Up To Date

Something has gone wrong, check that all fields have been filled in correctly. If you have adblock, disable it.

The form was sent successfully

What Matters

The Point

AI infrastructure has opened a part of China’s market that was not previously in our opportunity set, expanding what we can own and why.

The Proof

Export restrictions and a policy-mandated domestic buildout are creating structural demand in semiconductor equipment, cloud infrastructure, memory architecture, and data-movement technology in businesses the market still reads as cyclical manufacturers or substitution plays, and we read differently.

The Result

We have established early-stage positions across the infrastructure stack as exposure to an AI buildout that is longer, larger, and more equipment-intensive than most investors currently appreciate.

When DeepSeek released R1 in January 2025, we think Western markets asked the wrong questions. They wanted to know who lost and which stocks to sell. To us, the more interesting question was what a small research lab in Hangzhou had actually proved.

Founded in 2023 as a research arm of High-Flyer Capital, a Chinese quantitative hedge fund, the lab had no hardware advantage, no legacy infrastructure, none of the accumulated research its American peers had spent years building. On the quality of chips it had access to, DeepSeek should not have produced what it did. That it did anyway revealed something important about what Chinese engineering culture can do under pressure.

Once understood, the question became where else in Chinese technology the same dynamic was at work.

This is the question that took us to Beijing and Shanghai in early 2025. Not to evaluate the models. To understand the stack being built underneath them.

Five Moments That Changed the Conversation

R1 was the first signal.

The second came in late 2025, as Huawei captured share from NVIDIA in China’s artificial intelligence (AI) chip market and a wave of domestic graphics processing unit (GPU) designers, including Moore Threads, MetaX, Biren Technology, and Iluvatar CoreX, filed to go public in Hong Kong and Shanghai.

Early 2026 brought the third, when China approved initial public offerings for Zhipu (Z.ai) and MiniMax, two of its most prominent AI laboratories. We saw this as a clear statement from its capital markets about where long-term investment was heading. Meanwhile, Alibaba‘s Qwen and ByteDance continued to launch leading AI models at an accelerating cadence.

Then a wave of profitable A-share semiconductor companies began listing in Hong Kong. Montage Technology‘s Hong Kong shares now trade at a roughly 30% premium to its mainland shares, a reversal of the historical pattern and a likely sign of international investors’ conviction in leading Chinese semiconductor players.

The fifth and final moment came in May 2026, when CXMT and YMTC, China’s two leading memory producers, filed to go public. Memory is not a peripheral element of the AI story. It is structural. No model runs without it. No data center scales without it. No domestic AI ambition survives without a reliable local supply of it.

Read together, those five moments sketched for us the outline of something with real momentum.

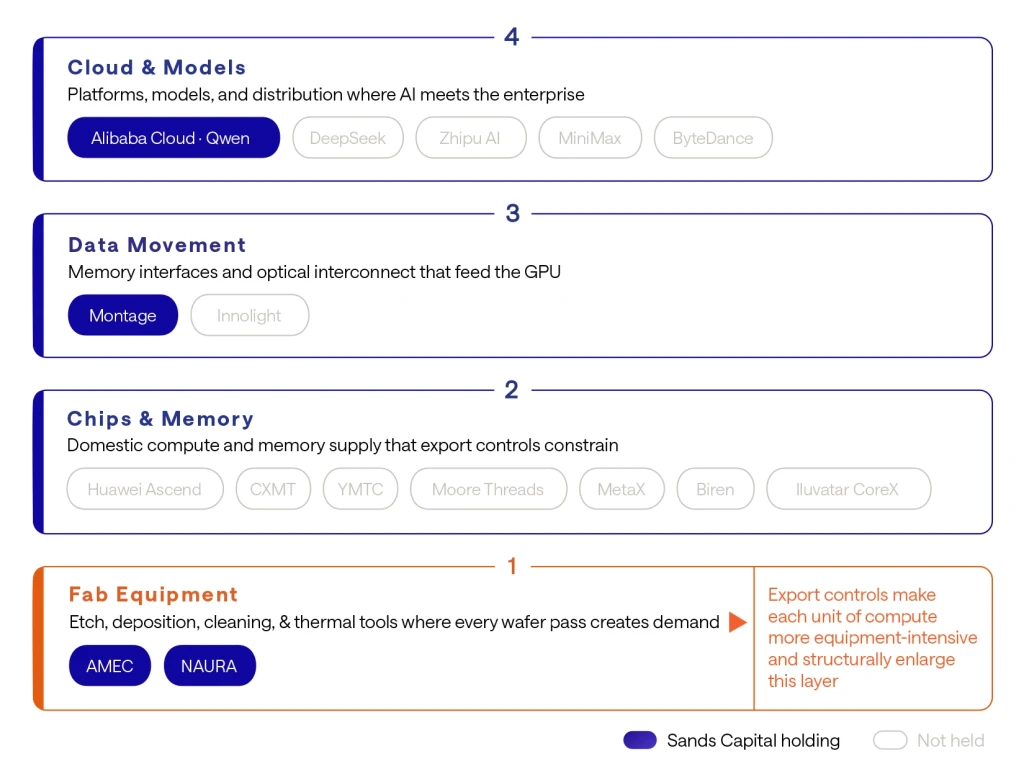

China’s AI Infrastructure Stack Takes Shape

China is moving through the early stages of an AI buildout with speed and internal coordination that is, whatever one thinks of the geopolitical context, genuinely impressive. It resembles the United States several years into its own infrastructure wave, but compressed, faster, and carrying the additional weight of having to build local alternatives to supply chains it can no longer take for granted.

A Decade of Looking at the Wrong Things

China’s technology sector spent a decade being easy to describe. Consumer internet defined it. Big ecommerce platforms. Social networks. Mobile payment systems that collapsed a generation of financial infrastructure into a few years.

The investors who saw those businesses early had the opportunity to do well, and their framework hardened into habit. It became the default lens through which much of the market read anything with a Chinese address, long after it had stopped being adequate.1

The research revealed a different map entirely.

The most consequential conversations were happening in semiconductor equipment facilities, in cloud infrastructure operations, in engineering corridors. We rarely saw them show up in investment presentations. Chinese technology’s energy has migrated. It now lives with manufacturers and process engineers, with people solving difficult physical problems rather than optimizing digital funnels. Many international investors have not followed it there.2

The state has, emphatically. China’s 15th Five-Year Plan names advanced manufacturing and AI infrastructure as central priorities through 2030. A fund targeting $138 billion across AI and robotics over 20 years is not a market bet.3 Neither is a $295 billion program to build a nationwide network of interconnected data centers, with at least 80 percent of the technology mandated to come from domestic suppliers.4 Together they describe a policy architecture with its own gravity, and the companies building inside it do not face the demand uncertainty that haunts early-stage technology investment in most other markets.

Today China has 602 million generative AI users, every one of them served by domestic platforms because foreign alternatives are inaccessible.5, 6 Over the same years that internet and software names struggled, hardware and semiconductor businesses moved sharply higher.

We do not read that divergence as a temporary rotation. It marks where durable demand has relocated, and the distance between where investor attention still concentrates and where the most interesting work is happening has not yet closed.

The Constraint That Built the Market

Start with the supply gap, because it explains what follows.

The United States and its allies will consume something like 12 million AI chips this year. China produces around 2 million domestically, against domestic demand that may already exceed 5 million units.7 That shortfall is not closing quickly, and it has injected an urgency into China’s domestic technology buildout that was audible in every meeting on the ground.

The Dutch company ASML makes the extreme ultraviolet (EUV) lithography machines on which modern chip fabrication depends. It cannot sell its most advanced deep ultraviolet (DUV) or any EUV systems to Chinese customers. Without them, Chinese fabrication plants work with older DUV equipment and compensate through multipatterning, a technique that reaches comparable transistor densities by layering additional process steps rather than using more precise optics.

It works. It also demands more etch passes, more deposition cycles, and more cleaning runs per wafer than the EUV route requires.

The consequence is structural. Producing a given unit of AI computing capacity in China consumes more semiconductor manufacturing equipment than producing the same unit in the West. Washington did not close down domestic chip production in China. It made the infrastructure supporting that production considerably larger.

That enlargement is where we found Advanced Micro-Fabrication Equipment.

Gerald Yin built AMEC, based in Shanghai, after years developing etch platforms at Lam Research in California. Etch tools cut the microscopic patterns that give a chip its function, and at the geometries advanced memory and logic now require, the tolerances are measured in atoms. Sustaining them across hundreds of thousands of production wafers is among the hardest challenges in manufacturing.

There is no shortcut. The knowledge accumulates through years of running tools in live environments, through failure modes that only surface at volume, through the slow layering of engineering insight that each wafer run deposits.

For years, Chinese equipment companies were locked out of that learning. Domestic fabs were too cautious and too small to provide the production access that builds real capability.

That has changed.

Fabs across China now run AMEC tools at a scale the company could not have accessed five years ago, and the knowledge compounding inside the business reflects it. Its most advanced tools address the NAND architectures China’s memory producers are scaling toward, and the 3D DRAM applications that could open a domestic path to high-bandwidth memory, today one of the most constrained inputs in China’s AI supply chain.

The significance of what AMEC builds does not rest only on what it replaces. It rests on what China still needs to make.

Breadth tells a different story, and an equally important one.

Beijing’s NAURA Technology is China’s largest semiconductor equipment manufacturer, not by depth in any single process, but by how much of the production floor it covers. Etch, deposition, cleaning, thermal processing. Five years ago, that range was a sensible portfolio. Today it is a strategic position.

The fabs scaling fastest across China want qualified local suppliers at every step, not just one or two. A company already embedded across multiple process stages has an intimacy with those customers that no single-process specialist can replicate. NAURA holds that position at precisely the moment when the next wave of domestic fab capacity begins to crest.8

Power, Cloud, and the Platform Question

Energy rarely appears in the China AI conversation, which is strange given how much it will eventually matter.

The United States leads in AI demand today, but China operates the world’s largest power grid, generating more than twice as much electricity as the United States.9 At sufficient scale, AI infrastructure runs into power ceilings as hard as chip ceilings. If domestic semiconductor production closes even a portion of the current supply gap, that latent power infrastructure could support a data center buildout that moves faster and reaches further than many outside observers have modeled.

Calling Alibaba an ecommerce company is like calling Amazon a bookstore. Accurate in a narrow historical sense, and practically misleading.

The Hangzhou company runs China’s largest cloud infrastructure platform by revenue, develops its own chips, and has invested in large language models and enterprise AI services at a depth that places it at the center of how Chinese businesses deploy AI in production today. Its Qwen model family offers open weight and closed-weight models and is gaining credibility well beyond China. Western companies have started using it, drawn by the speed and the economics.

Most investors still reach for the retail narrative when they price the stock. The question that we believe will matter over the next decade is not who wins Chinese ecommerce. It is who owns the infrastructure on which Chinese AI runs, and that answer runs through Alibaba in ways the market has not yet absorbed.

Up the Stack

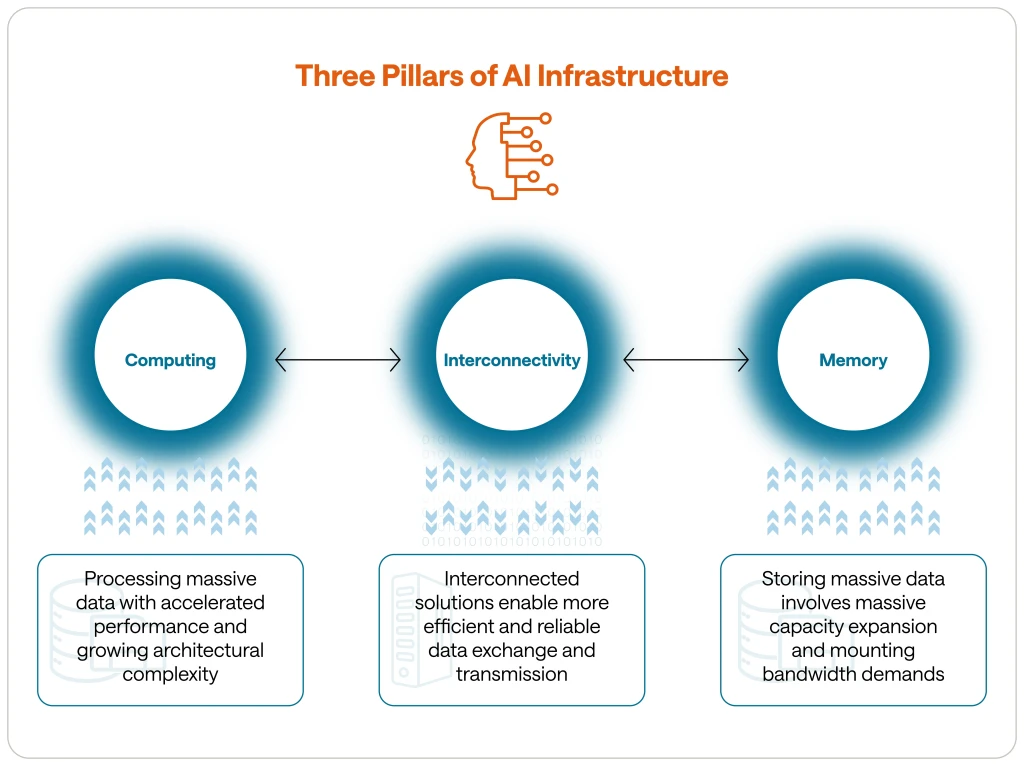

Compute commands most of the attention in AI infrastructure investing, and reasonably so. But as systems scale, constraints migrate. Memory bandwidth, the efficiency with which data moves between processors and storage, the speed at which compute nodes communicate with one another, these become binding.

The GPU earns the headline. The plumbing that feeds it quietly determines what the system can actually do.

AI infrastructure rests on three pillars. Compute, memory, and interconnect. The first two attract almost all the attention. The third is where Montage Technology operates, and where we believe some of the most durable value in this cycle will be created. We found our way to the company through the co-founders themselves, in Shanghai, rather than through the usual channels.

Montage is the No. 1 by market share revenue memory interface chips supplier globally, the semiconductors that govern how data moves between processors and memory inside AI servers. It holds roughly one-third of the global market in an oligopolistic industry where products sit in mission-critical parts of the server architecture, require extensive qualification, and carry long product lifecycles. Switching costs are real and rising.10

Three pillars of ai infrastructure: computing, memory and interconnectivity

The company also sits on the board of the Joint Electron Device Engineering Council, one of a small number of trusted vendors helping shape the industry standards its own products must meet, alongside deep ecosystem relationships with Samsung Electronics, SK hynix, and Micron Technology.

What makes the position especially compelling is the direction of travel. As AI training and inference workloads scale, signal integrity, latency, bandwidth, and power efficiency are becoming system bottlenecks that no amount of additional compute resolves on its own. Montage is expanding beyond memory interface into peripheral component interconnect express, optical, and Ethernet interconnect, precisely the areas where higher bandwidth demand is accelerating innovation.

The company is not just the incumbent leader in one part of the interconnect layer. It is positioning itself across the layer at the moment when that layer is becoming the binding constraint on AI system performance.

As models grow larger and inference workloads grow more complex, that flow becomes as important to system performance as the processors themselves. It is an unglamorous problem with large consequences, and Montage has spent years becoming an expert at solving it in a corner of the market where very few investors are looking.11

Fast memory solves part of the problem. Fast connections between servers solve the rest.

That is why we view Montage as more than a narrow component supplier. The company sits at a pressure point where compute, memory, and data movement meet. As AI workloads become more demanding, the ability to move data efficiently inside the server becomes increasingly important to overall system performance. This is a quieter part of the AI stack, but one that we believe should become more valuable as China scales domestic AI infrastructure.

What We See That Others May Not

Many investors approaching China’s AI infrastructure story could read it as a story about restriction. American export controls created demand for domestic alternatives, Chinese companies stepped in to fill the gap, and the investment case rests on how long policy support holds.

The reading is not wrong. It is just incomplete, and the part it misses is where we believe the real long-term value lies.

AMEC is an example of why.

The market prices it as a domestic substitute for Lam Research, a company that earns margin as long as Western competitors remain restricted. We see something different. Yin did not build AMEC to fill a gap. He built it to build world-class etch tools, and the company’s engineering culture reflects that ambition in our view.

What we believe makes AMEC special is what happens to its tools over time. Every wafer run adds to an accumulating base of process knowledge that makes the next tool better than the last. That learning curve is not available to a new entrant. It cannot be purchased or reverse engineered. It compounds quietly, year after year, inside the installed base. The deeper that base grows, the harder the competitive position becomes to challenge, and the more valuable AMEC’s relationships with the fabs that depend on its process expertise should become.

This is not only a substitution story. It is a moat in formation.

NAURA is a different kind of moat but an equally durable one.

Its value does not come from being the best at any single process. It comes from being qualified across many of them. A fab that has embedded NAURA tools across etch, deposition, cleaning, and thermal processing has built a relationship of operational dependency that can take years to replicate with another supplier.

As China’s fabs grow more sophisticated and their production processes grow more complex, the cost of switching away from a multistep qualified supplier rises. NAURA’s breadth, which the market may read as a sign of being a generalist rather than a specialist, is what we see as the source of its pricing power and customer retention. That advantage deepens with every new process step it qualifies.

Alibaba’s long-term value creation story is perhaps the most misread of the group.

The market has spent years discounting the stock for its ecommerce exposure, its regulatory history, and its complexity. What it has consistently underweighted is the compounding nature of cloud infrastructure businesses.12 Alibaba Cloud does not just sell compute. It sells the accumulated data relationships, enterprise integrations, developer tools, and AI model capabilities that make switching costs real and rising.

Every Chinese enterprise that builds its AI stack on Alibaba Cloud deepens a dependency that competitors cannot easily displace. Qwen is not just a model. It is a distribution mechanism that extends Alibaba’s infrastructure reach into organizations that may not have been cloud customers a few years ago.

We expect that the business that emerges from this cycle will look less like an ecommerce company and more like the indispensable infrastructure layer of the Chinese digital economy. That transformation is still early, and the market is likely still pricing the old story.

Montage is where the research process itself created the edge.

The company’s co-founders are not well known outside a narrow circle of semiconductor professionals. The problem they are solving, memory interface efficiency at the scale AI demands, does not appear in many AI infrastructure investment frameworks.

Time spent in Shanghai understanding it from first principles made clear to us that Montage occupies a position in the AI stack that becomes more valuable, not less, as AI systems grow more capable and more demanding. The memory bandwidth problem does not go away. It intensifies with every new model generation, every expansion of context length, every increase in inference complexity.

A company that has spent years accumulating the engineering expertise to solve it, in a market where few others are focused, could have the kind of early-mover advantage in a critical chokepoint that long-term investors look for. The multiple it trades at today does not reflect what we expect the multiple could look like in we expect five years if AI scales the way we believe it will.

The Geopolitical Layer

China’s government has grown visibly more protective of its AI infrastructure as that infrastructure has grown more valuable. There are credible reports of authorities intervening after attempts to move AI talent and intellectual property abroad through Singapore-based vehicles. Restrictions on staff at major Chinese AI firms are discussed openly in investment circles.

This sector is no longer treated as commercial infrastructure alone. It is strategic, and the policy environment manages it accordingly.

We believe this reality shapes how positions are sized, which businesses benefit from proximity to state priorities and which risk being constrained by them, and the scenarios where the industrial logic holds but the investment becomes difficult to execute regardless.

It does not alter our core observation. Something large is being built here. The people building it are capable and determined. The businesses supplying the infrastructure beneath it are earlier in their opportunity than market pricing currently reflects.

The View From the Factory Floor

The substitution narrative is not wrong. Export restrictions created genuine demand for domestic alternatives, and the companies meeting that demand are real businesses with real revenues.

As a thesis, however, it is thin. It reads the opportunity as a function of what was restricted rather than what is being built. To us, those are different stories, with different durations and different eventual magnitudes.

The engineering culture that produced R1 did not emerge from nowhere, and it did not stay in Hangzhou.

It is present in how AMEC’s engineers describe the slow, iterative work of making their tools more reliable. It lives in the ambition of NAURA’s platform strategy, in the patient seriousness with which Montage’s founders approached a problem, requiring more than a decade of technological iteration, that a lot of the market has not yet named. It shows up in the way Alibaba is repositioning from consumer platform toward the cloud and model infrastructure required to serve enterprise AI demand at scale.

The more important question is not whether Chinese models outperform American models next quarter. It is, we believe whether China can build the infrastructure required to support AI deployment at scale without depending on supply chains it cannot control.

Its own chips. Its own memory. Its own cloud. Its own infrastructure stack.

That project is already underway.

Many of the businesses we own sit at important points in that stack. Each occupies a position that becomes more strategically important as the buildout deepens, with competitive advantages we believe the market is not yet pricing correctly. What drew us to this part of the market was not the geopolitical narrative or the policy tailwind alone. It was the quality of the businesses themselves, the depth of the moats forming inside them, and our conviction that patient, long-term investors who understand them early may find some of the more consequential opportunities in China today.

1. SoftBank’s $20 million investment in Alibaba in 2000 was valued at approximately $58 billion at the time of Alibaba’s IPO filing in 2014 (Bloomberg, May 7, 2014). Naspers’s $32 million stake in Tencent, acquired in 2001, was valued at $175 billion when Naspers sold a partial position in 2018 (Bloomberg, March 22, 2018). Sequoia Capital’s $60 million investment in WhatsApp returned approximately $3 billion — a 50x multiple — when Facebook acquired the company in 2014 (TechCrunch, February 19, 2014).

2. https://www.atlanticcouncil.org/blogs/econographics/chinas-stock-market-collapse-is-the-end-of-the-road-for-many-foreign-investors/

3. “China to Invest 1 Trillion Yuan in Robotics and High-Tech Industries”, IFR, Mar 25, 2025. URL:https://ifr.org/ifr-press-releases/news/china-to-invest-1-trillion-yuan-in-robotics-and-high-tech-industries?cs=0&hl=en-US&biw=1920&bih=911

4. “China Preps $295 Billion Plan to Fund Nationwide AI Buildout,” Bloomberg News, June 9, 2026. URL: https://www.bloomberg.com/news/articles/2026-06-09/china-prepares-295-billion-plan-to-fund-nationwide-ai-buildout

5. https://www.globaltimes.cn/page/202602/1354857.shtml

6. https://dig.watch/updates/china-leads-the-global-generative-ai-adoption-with-515-million-users

8. https://www.reuters.com/world/china/china-mandates-50-domestic-equipment-rule-chipmakers-sources-say-2025-12-30/

9. https://www.wsj.com/tech/china-ai-electricity-data-centers-d2a86935

10. From Frost & Sullivan cited in the February 2026 IPO prospectus Montage’s HK IPO Prospectus (February 2026).

11. https://medium.com/@kvnagesh/the-quiet-evolution-of-memorys-critical-infrastructure-8b407fb39638

12. Alibaba Group Holding Ltd., Form 6-K, filed November 2025 (quarter ended September 30, 2025). Cloud segment grew 26% year over year; AI-related revenue sustained triple-digit growth for the eighth consecutive quarter and represented approximately 20% of external cloud revenue. Management noted over 180,000 derivative models built on the Qwen family as of October 31, 2025, more than double the second-largest provider. China AI cloud market share of 35.8% per Omdia, “AI Cloud Market: China – 1H25,” as cited therein.

Disclosures:

The views expressed are the opinion of Sands Capital and are not intended as a forecast, a guarantee of future results, investment recommendations or an offer to buy or sell any securities. The views expressed were current as of the date indicated and are subject to change.

This material may contain forward-looking statements, which are subject to uncertainty and contingencies outside of Sands Capital’s control. Readers should not place undue reliance upon these forward-looking statements. There is no guarantee that Sands Capital will meet its stated goals. Past performance is not indicative of future results.

All investments are subject to market risk, including the possible loss of principal. Recent tariff announcements may add to this risk, creating additional economic uncertainty and potentially affecting the value of certain investments. Tariffs can impact various sectors differently, leading to changes in market dynamics and investment performance.

As of June 11, 2026, Advanced Micro-Fabrication Equipment, Alibaba, Amazon, ASML, Contemporary Amperex Technology, Lam Research, Micron Technology, Montage Technology, NAURA Technology, NVIDIA, Samsung Electronics, and SK hynix were held across Sands Capital strategies. The companies identified represent a subset of current holdings and were selected by the author on an objective basis to illustrate the views expressed in the commentary.

Any holdings outside of the portfolio that were mentioned are for illustrative purposes only.

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. There is no assurance that any securities discussed will remain in the portfolio or that securities sold have not been repurchased. You should not assume that any investment is or will be profitable.

References to the “firm”, “we” or “our” are references to Sands Capital. Sands Capital refers to the combination of Sands Capital Management, LLC, Sands Capital Alternatives, LLC and Sands Capital Horizons, LLC. All three firms are registered investment advisers with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. The three registered investment advisers share certain personnel, office space, and other resources.

This communication is for informational purposes only and does not constitute an offer, invitation, or recommendation to buy, sell, subscribe for, or issue any securities. The material is based on information that we consider correct, and any estimates, opinions, conclusions, or recommendations contained in this communication are reasonably held or made at the time of compilation. However, no warranty is made as to the accuracy or reliability of any estimates, opinions, conclusions, or recommendations. It should not be construed as investment, legal, or tax advice and may not be reproduced or distributed to any person.