Related Articles

Stay Up To Date

Something has gone wrong, check that all fields have been filled in correctly. If you have adblock, disable it.

The form was sent successfully

What Matters

The Point

Lower launch costs are reshaping the economics of orbit and opening the earliest investible opportunities across launch-adjacent infrastructure, spacecraft, mission systems, communications, sensing, and defense-linked capabilities.

The Proof

Cheaper, more frequent, and more reliable access to space is driving higher orbital activity and giving the businesses closest to that shift a clearer path to commercial traction.

The Result

Over time, the greatest value may accrue to companies that translate a more active orbital economy into durable revenue, stronger competitive positions, and attractive returns on capital.

From the California coast, a SpaceX launch begins as a distant brightness and then becomes something physical. First comes the hard white-orange flare beneath the rocket. Then comes the sound, building from a sharp crackle into a deep rolling force that lands in the chest as much as the ear. For a few seconds, the whole scene feels suspended between precision and violence.

What stayed with us was not simply the spectacle, but the economics behind it.

SpaceX changed the game for the space industry. By lowering the cost of reaching orbit and improving launch cadence and reliability, the company began to remove the constraint that had limited commercial activity in space for decades.

That matters not only for engineers or governments, but for long-term investors. When access becomes cheaper and more dependable, more businesses can be built on that foundation. Some will grow. A smaller number may be durable enough to earn attractive returns on capital.

Assessing the New Space Paradigm

We have studied paradigm shifts like this before, including the move from mainframes to personal computers (PCs), the widespread adoption of mobile devices, and the migration to cloud computing. Across industries, the breakthrough itself is rarely the whole story. What matters is the ecosystem that forms around it.

Across industries, the breakthrough itself is rarely the whole story. What matters is the ecosystem that forms around it.

When Steve Jobs unveiled the iPhone in 2007, most people could not yet imagine how a smartphone that replaced buttons with a touch interface would, over time, become the control center for so much of daily life. Few envisioned how that device would support more than 2 million applications engineered, in their most basic sense, to solve a problem, answer a question, or automate a process.

Gradually, people could order food, book air travel, find dates, and navigate backroads and byways through a digital device, giving rise to new business models and companies such as Shopify and DoorDash. More recently, artificial intelligence has widened what can be built and where value can accrue across software and digital infrastructure.

Space may now be entering a similar phase. However, when and how extensively we could see this develop remain unclear. Lower launch costs are not simply improving an existing system. Launch now acts as an infrastructure layer that can serve as the foundation for what can be deployed, sustained, and built profitably in orbit.

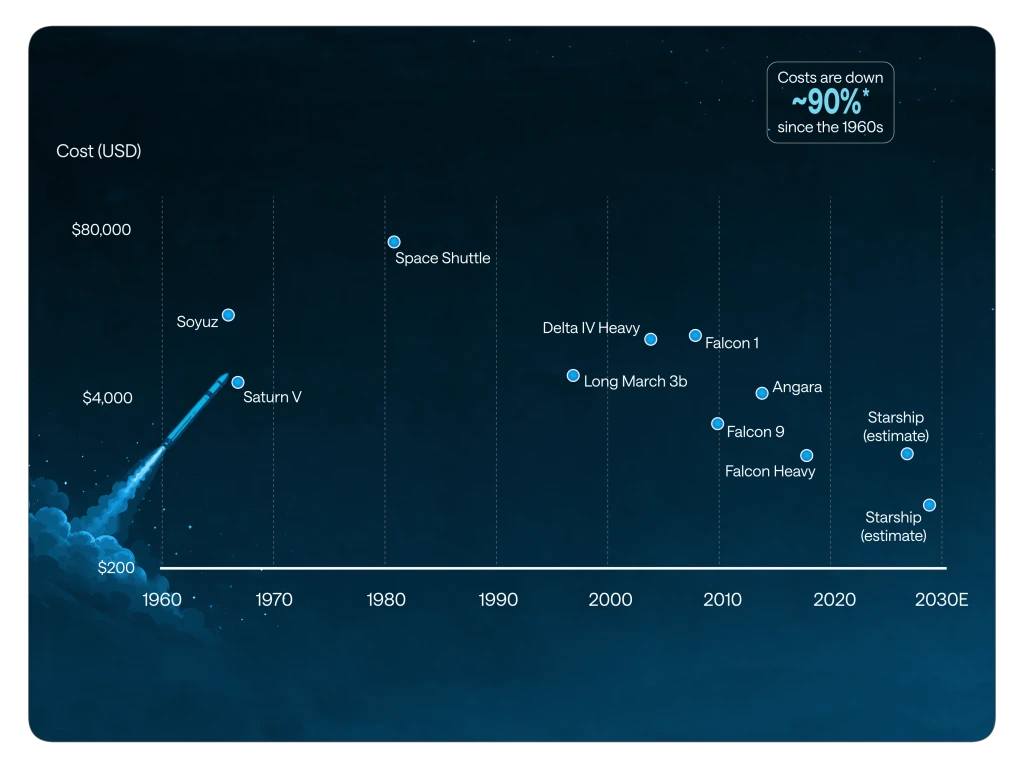

THE FALLING COST OF REACHING SPACE

Launch Cost per Kilogram of Payload

Investibility Improves as Launch Costs Fall

For decades, space sat just beyond the boundary of straightforward investment analysis. The technology was extraordinary. The strategic relevance was obvious. The economics were far less clear.

High costs, heavy government dependence, long development cycles, and uncertain commercial returns kept the category closer to engineering excellence than durable business formation.

Today, the investibility of space is improving because the economics are changing in ways that are becoming easier for public markets to understand. In the Space Shuttle era, NASA estimated launch costs at roughly $1.5 billion per mission, or about $54,500 per kilogram to low Earth orbit. By comparison, NASA has cited Falcon 9 at roughly $2,720 per kilogram based on earlier published pricing, while SpaceX’s current launch materials list Falcon 9 at $74 million per mission through 2026.1

Much of this future depends on the cost of sending rockets into space continuing to fall. In the past 15 years, launch costs have dropped from $50,000 per kilogram to under $2,000. They are expected to dip below $200 per kilogram with Starship, which is a reusable, heavy-lift launch vehicle being developed by SpaceX.2

Reusability has been central to that shift. SpaceX describes Falcon 9 as the world’s first orbital-class reusable rocket and explicitly links reflight to lower space-access costs.3 At the same time, the installed base in orbit has expanded sharply. The European Space Agency (ESA) says about 40,000 objects are now tracked in Earth orbit, including roughly 11,000 active payloads, which means the opportunity is no longer limited to launch alone but increasingly extends to communications, software, data, tracking, and other space-enabled services.4

A Market Entering Its Growth Phase

The market is beginning to reflect that shift. McKinsey & Company placed the global space economy at about $630 billion in 2023 and projected it could reach close to $1.8 trillion by 2035.5

That broader ecosystem is part of why a potential SpaceX initial public offering (IPO) matters so much. As of April 30, 2026, the company has not announced the date of its IPO. However, rumors of IPO preparations and discussion of a very large valuation have already helped shift investor psychology. A public SpaceX would likely be viewed not simply as a launch company, but as a visible marker that space has moved from a speculative frontier toward a market investors can price through the lens of scale, margins, and optionality.

If that happens, the effects may extend beyond SpaceX itself, drawing more capital and attention toward adjacent companies whose economics could improve further if Starship is able to further lower costs. The Starship spacecraft is designed to sit on top of a super heavy booster and is designed to be a fully reuseable system for carrying cargo and people to Earth orbit, the Moon, and beyond. SpaceX describes it as the most powerful launch vehicle it has developed, with a planned payload of up to 150 metric tons when fully reusable and 250 metric tons in expendable mode.6

In that sense, SpaceX may mark a turning point not only in the cost of accessing space, but in how investors value the broader space economy.

Constellations (a cluster of satellites) become easier to deploy. Hardware can be refreshed more often. Systems can be designed to evolve rather than merely survive. Orbit begins to look less like a distant mission domain and more like infrastructure.

Extending the Investible Universe

The opportunity, then, is better understood not as a wager on space in the abstract, but as an investment case built on a developing industrial system. Launch is the foundation, but the investible surface extends well beyond it into spacecraft, satellites, manufacturing, mission systems, communications, sensing, software, and, over time, the services required to support a denser orbital environment.

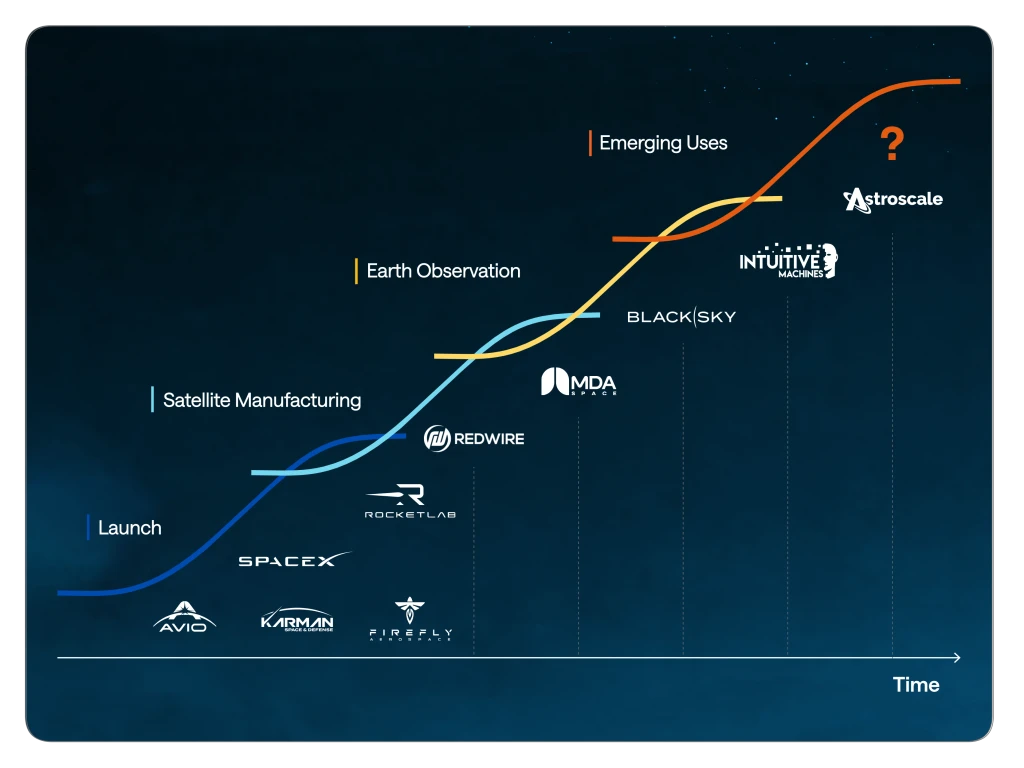

APPLYING THE FRAMEWORK TO SPACE

Seen this way, the category begins to evolve into layers. At the base is launch and transport, the access layer that makes everything else possible. Above that sits spacecraft and manufacturing, including satellite buses, propulsion systems, sensors, avionics, communications hardware, and integration services. Higher up are orbital platforms and constellations such as broadband networks, Earth observation systems, navigation and timing architectures, and defense-related systems. SpaceX’s Starlink, for example, is a large low Earth orbit constellation. It surpassed 10,000 satellites in orbit as of March 2026, a number that would have been difficult to imagine a decade ago.7

Beyond those layers sit the data and application businesses that convert orbital assets into usable services on Earth. Still further out are newer categories such as in-orbit servicing, debris mitigation, traffic management, and cislunar logistics.

This layered view imposes useful discipline. Not every layer is equally mature. Not every layer is equally investible.

Space manufacturing may be one of the most intriguing frontiers in the orbital economy. The idea is not just to launch hardware into space, but to use microgravity itself as a manufacturing advantage. Redwire is already exploring that possibility across pharmaceuticals, industrial materials, and tissue bioprinting. Its successful 3D bioprinting of a human knee meniscus on the International Space Station is the kind of milestone that expands what investors can plausibly imagine. It suggests that orbit may eventually become more than a destination for satellites and missions. It may become a place where high-value products are actually made.

The commercial case is becoming easier to see in some parts of the space economy. MDA Space, which supplies satellites, robotics, and geointelligence capabilities, has grown revenue more than 200 percent since 2021. BlackSky, which delivers real-time satellite imagery and analytics to help customers monitor critical locations and events, has increased revenue by roughly the same amount over the same period.8 They are different businesses at varying stages of maturity, but the direction is similar. In parts of the market tied to national security, surveillance, and data, demand is no longer abstract. It is beginning to show up in sustained revenue growth.

Others, such as in-orbit servicing and cislunar logistics, still depend on further technical progress and a denser orbital economy. Early efforts include Intuitive Machines, which is helping build a logistics layer between Earth and the moon, and Astroscale, the orbital servicing and debris-removal company.

Moonshot to Market

Public discussion of space still gravitates toward its most dramatic possibilities. Lunar infrastructure, orbital manufacturing, tourism, and in-orbit service economies attract attention because they feel like the future is arriving early.

However, we think the first investible area of the space economy is much closer to home.

That became clearer on the factory floor. At Rocket Lab’s facility in Long Beach, California, the setting is not cinematic. From the outside, the facility looks like a typical industrial warehouse.

Inside, it opens into a high-ceilinged, brightly lit manufacturing floor organized into distinct zones, including a 3D printing area, a clean room, and a quality station. The environment is ordered and precise. What stands out is not spectacle, but the disciplined repetition required to make complex systems reliable.

That fieldwork has to a certain degree changed how we are assessing the investible market. The relevant question is no longer who can evoke the future most vividly, but who is building the capability to sustain it.

On the ground, the category begins to resemble other advanced industrial systems, shaped by throughput, quality control, integration, and operational rigor. The more useful questions become familiar ones. Who is building repeatable systems? Who is solving mission-critical problems? Who occupies the part of the stack where demand is likely to deepen first?

In the near term, that points most clearly to launch-adjacent infrastructure, spacecraft, satellite components, mission systems, communications, sensing, and selected defense-linked capabilities. The most compelling opportunities today are not necessarily the most futuristic. They are the businesses already benefiting from rising orbital activity and improving launch economics while supplying capabilities customers need now.

The Businesses Closest to the Shift

Once the layers are clear, the company picture becomes easier to interpret. SpaceX has reset the baseline for the industry, but it is not yet a public company. For investors, the more relevant question is which businesses are positioned to benefit as the system broadens.

Rocket Lab is one example of a company participating across multiple layers. The company is not trying to compete on launch alone. It has built a broader position across launch, spacecraft, and satellite components. That matters because pure launch is likely to remain a difficult business, with visible pricing, high capital intensity, and little room for error.

The company’s recent results support that view. In 2025, Rocket Lab flew 21 missions and generated $602 million of revenue, including $180 million in the fourth quarter, representing 38 percent growth year over year.9

Those figures matter less as a snapshot than as evidence that the business is already becoming more than a launch provider. If orbit continues to industrialize, companies that participate across more than one layer of the stack may become more resilient than those exposed to launch alone.

MDA Space offers another useful example of that broadening stack. The company is not exposed to launch economics in the same way. Instead, it sits across satellite systems, robotics, and geointelligence, areas that should benefit as orbital infrastructure becomes more complex and more commercially relevant. Its 2025 results were strong, with revenue rising 51 percent to C$1.63 billion. That profile looks different from launch. It points instead to the value of owning pieces of the architecture that make orbit more functional, more intelligent, and more useful.10

Avio presents a different but equally relevant angle. With roots dating back to the early 20th century, the Italian company sits at the intersection of launch and defense. Its expertise in solid rocket motors places it at the core of Europe’s launch and propulsion ecosystem.

That positioning matters because demand in this part of the market is already visible and anchored by institutional customers, such as the ESA, which account for roughly 80 percent of Avio’s space backlog. It may strengthen further as European defense spending accelerates, and space capabilities become more strategically important. EU defense spending reached €343 billion in 2024, up 19 percent year over year. The European Commission’s ReArm Europe Plan/Readiness 2030 aims to mobilize up to €800 billion for defense investment. With space now identified as a priority area and NATO targeting 5 percent of GDP in defense and security-related spending by 2035, the demand backdrop could become stronger still.11

Astroscale belongs in the discussion as well, though in a different part of the curve. Its servicing and debris-removal work offers a glimpse of a later layer of the orbital economy. As more valuable assets populate orbit, services such as debris monitoring, collision avoidance, in-orbit inspection, refueling, maintenance, and end-of-life management become easier to justify. Consider, between 2017 and 2022, the number of monthly near misses between satellites and debris within 1 kilometer of each other went from 1,500 to 5,800.12 The example matters not because it demonstrates that this market is ready today, but because it suggests what a denser and more active orbital environment may eventually require.

The fieldwork sharpened these distinctions. Rocket Lab appears to offer an example of a broadening commercial stack. Avio seems more tied to institutional demand and defense-linked programs. Astroscale points toward a later service layer that may become important as orbital density increases. The opportunity set is not uniform, and that is precisely why selectivity matters.

From Frontier to Investment Analysis

For longer-term investors, that is the larger point. Space is becoming less a story of technological spectacle and more a story of infrastructure, industrial capability, and strategic relevance.

The opportunity will not be defined by the boldest concept or the furthest horizon. We believe it will be defined by which businesses can translate a more active orbital economy into durable revenue, stronger positions in the value chain, and attractive returns on capital.

Scarcity defined the earlier era. Scale may define the next one. That does not make every part of space investible today. It does suggest that the category is beginning to move from fascination to investible sector. That is usually the point at which a frontier starts to become a market.

1. https://www.spacex.com/assets/media/Capabilities&Services.pdf

3. https://www.spacex.com/vehicles/falcon-9

4. https://www.esa.int/Space_Safety/Space_Debris/ESA_Space_Environment_Report_2025

6. https://www.spacex.com/vehicles/starship

8. Revenue growth is not a predictor of stock price or investment performance and was sourced from MDA Space and BlackSky.

10. https://mda-en.investorroom.com/financial-documents

12 https://payloadspace.com/a-satellite-conjunction-scare-marks-an-inflection-point-in-collision-risk/

Disclosures:

The views expressed are the opinion of Sands Capital and are not intended as a forecast, a guarantee of future results, investment recommendations or an offer to buy or sell any securities. The views expressed were current as of the date indicated and are subject to change. This material may contain forward-looking statements, which are subject to uncertainty and contingencies outside of Sands Capital’s control. Readers should not place undue reliance upon these forward-looking statements. All investments are subject to market risk, including the possible loss of principal. Recent tariff announcements may add to this risk, creating additional economic uncertainty and potentially affecting the value of certain investments. Tariffs can impact various sectors differently, leading to changes in market dynamics and investment performance.

As of April 28, 2026, Shopify and DoorDash are held across Sands Capital portfolios. These companies were selected on an objective basis to illustrate examples of companies that utilize digital infrastructure.

Any holdings outside of the portfolio that were mentioned are for illustrative purposes only.

The specific securities identified and described do not represent all the securities purchased, sold, or recommended for advisory clients. There is no assurance that any securities discussed will remain in the portfolio or that securities sold have not been repurchased. You should not assume that any investment is or will be profitable.

Sands Capital refers to the combination of Sands Capital Management, LLC, Sands Capital Alternatives, LLC and Sands Capital Horizons, LLC. All three firms are registered investment advisers with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. The three registered investment advisers share certain personnel, office space, and other resources.

This communication is for informational purposes only and does not constitute an offer, invitation, or recommendation to buy, sell, subscribe for, or issue any securities. The material is based on information that we consider correct, and any estimates, opinions, conclusions, or recommendations contained in this communication are reasonably held or made at the time of compilation. However, no warranty is made as to the accuracy or reliability of any estimates, opinions, conclusions, or recommendations. It should not be construed as investment, legal, or tax advice and may not be reproduced or distributed to any person.