Related Articles

Stay Up To Date

Something has gone wrong, check that all fields have been filled in correctly. If you have adblock, disable it.

The form was sent successfully

AI uncertainty has put a cloud over software. The rapid improvement in AI’s capabilities, especially in code generation, is undeniable. We agree with the market’s assessment that AI is a disruptive force in the world of software. As a result, we need to maintain a higher bar for investments in this industry.

However, the current sell-off in software largely lacks nuance, with the entire sector being punished. In our view, this creates opportunities for long-term investors willing to think more deeply about which software companies may be capable of not only surviving in an AI world but thriving.

Key Points

- The market has severely punished software stocks recently due to advances in AI. However, we believe the indiscriminate selling misses important distinctions within software.

- We believe businesses in cybersecurity, infrastructure, and certain vertical software providers will have more AI opportunities with less AI-related risk than many peers in horizontal applications (e.g., a software-as-a-service (SaaS) application selling a sales or work management tool broadly across customer industries). However, even within this latter category, there are distinctions to be made with regard to systems of record versus systems of engagement, the types and size of customers, and the complexity of the problem being solved.

- We are concentrated, long-term investors, and can be selective in how we approach this broad sector. We believe the market’s indiscriminate view of the industry can create opportunities for long-term wealth creation by narrowing in on the businesses most likely to succeed.

Since the emergence of ChatGPT in 2022, investors have debated how artificial intelligence (AI) might reshape the software landscape. Early optimism about what AI could do for the sector centered on its potential to boost productivity, lower development costs, and help leading software companies extract more value from their large customer bases. That optimism has since given way to significant skepticism, with AI capabilities advancing rapidly and AI agents creating an entirely new innovation avenue. Agentic coding has moved forward the fastest. We believe tools, such as Anthropic’s Claude Code, have demonstrated to be impressive and seem to have significantly lowered the barriers and costs to writing code.

As a result, investors are increasingly concerned that this will lower barriers to entry and create new competition for incumbents, including competition for enterprise workloads from the large language model (LLM) providers themselves. Additionally, there is concern that AI will automate more job functions, leading to a smaller addressable market for software vendors selling on a seat-basis. With the rapid pace of exponential change, investors are uncertain about what the software landscape will look like in the future. The exponential pace of AI-driven change has made it difficult for investors to assess the durability of future cash flows across software businesses. This heightened uncertainty has led to valuation compression and broad-based selling pressure, often without differentiation between business models.

We are aware of these risks and remain in awe of what we see as the exponential pace of AI progress. However, we do not believe that AI’s impact will be uniform across software. The software industry has undergone multiple periods of innovation and disruption over the past several decades. History repeatedly shows that periods of heightened uncertainty tend to widen the gap between narrative and fundamentals. For some companies, a technological revolution can be extremely disruptive. For others, a sustainable innovation could make their product more valuable for customers and improve business. As long-term investors focused on high-conviction portfolios, we see opportunity in this disconnect.

Assessing the Impact

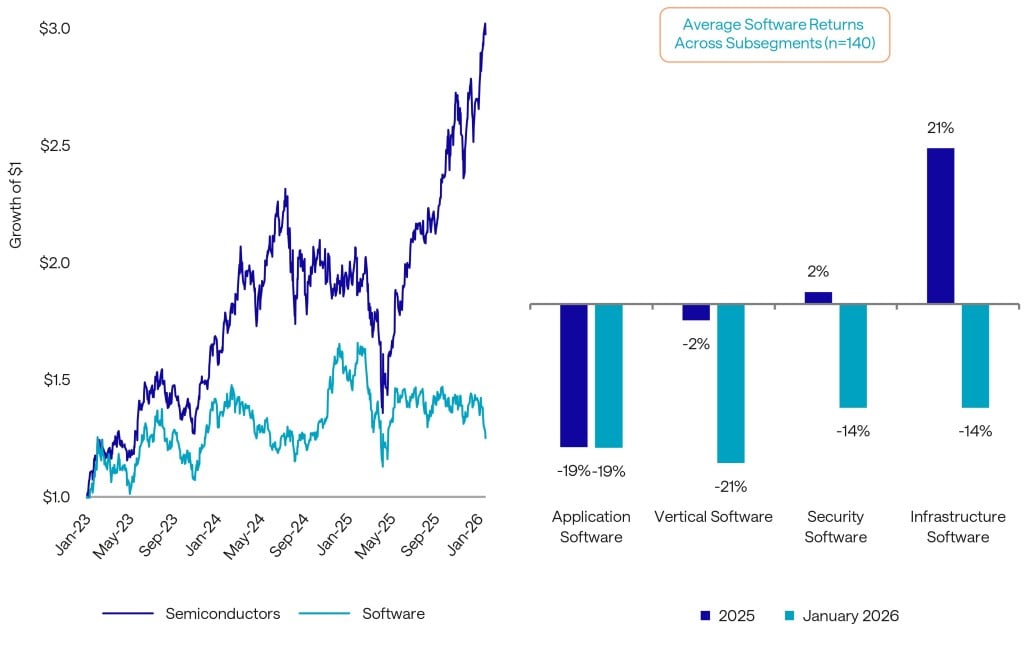

Exhibit 1

A BROADENING SELL-OFF IN SOFTWARE HAS EXACERBATED THE TECH DIVIDE

Evaluating AI Risks in Software

There are several key concerns that have become a focal point for investors:

- Competitive risks are top of mind for investors as AI lowers barriers to entry and reshapes application development. Easier access to coding tools could increase competition for incumbents, while vibe coding, or coding with plain language descriptions, raises the possibility that customers replace established third-party software vendors with internal solutions. At the same time, LLM providers may move up the stack into application layers, creating new sources of competition.

- Addressable market concerns stem from a view that traditional software may capture less of the go-forward opportunity as AI agents proliferate and eat into the traditional software total addressable market. This implicitly puts more pressure on incumbent vendors to create compelling agentic AI products. Additionally, if AI successfully automates more jobs, employers may elect to harvest those efficiency gains with layoffs, shrinking the number of seats needed from SaaS vendors.

- Business model risk reflects uncertainty about the current monetization mechanism for many software companies, which is seat-based licenses determined by how many people use the product. Investors question whether incumbents can shift from seat-based pricing toward hybrid- or consumption-based models to offset what could be a multidecade headwind on white-collar employment.

- The innovator’s dilemma adds structural risk for incumbents who have largely built their platforms upon deterministic workflows and traditional machine learning. These incumbents also have high margins that they may need to sacrifice to innovate in a new AI paradigm. Adding to this risk, these incumbents were not born in the age of AI. They all have some level of tech debt versus the startups building natively for this new paradigm.

We believe that the LLM providers themselves, such as OpenAI and Anthropic, create the most uncertainty and risk within the ecosystem. These companies are rapidly iterating from question-and-answer chatbots to autonomous agents that can complete ever more complex tasks. Most recently, Anthropic’s Claude Code has not only seen step function improvements in the software it can build but is seeing a proliferation of adoption and use cases well beyond developer coding, such as enabling non-technical employees to build their own. Its recently launched Claude Cowork platform extends these capabilities further and, impressively, it was written by Claude Code itself. We believe this emerging recursive capability should lead to an even faster cadence of innovation from Anthropic.

Despite these improvements, we still feel the market’s “shoot first and ask questions later” response will miss value-creation opportunities, even with some of the horizontal SaaS applications deemed most at-risk. Some of these are mission-critical systems of record supporting complex business logic that requires deterministic, precise outputs versus probabilistic predictions. These are sticky applications that can be extremely difficult to migrate away from without creating business continuity risk. Ironically, we have seen LLMs using the very services they are alleged to be disrupting, such as Atlassian, Asana, Anaplan, Datadog, Figma, HubSpot, GitHub, Qualtrics, Salesforce, and Workday. There is a difference between building a lightweight user interface with an agent and running a complex, scaled application with millions of users, 99.99 percent up-time, and security and governance controls. These SaaS vendors are also building their own AI capabilities into their products, often by using the models provided by OpenAI, Anthropic, and other leading LLMs. Lastly, enterprise software goes through complex sales cycles as a form of risk avoidance. Enterprises don’t want to invest large sums of money in complex software after only a weekend of evaluation, negotiation, and implementation.

As new entrants proliferate, we believe this dynamic helps reinforce the distribution advantages of the current leaders. The last debate concerns SaaS disintermediation by AI agents built on LLMs, which we believe is overstated but nuanced. In our view, the agents from Anthropic, OpenAI, and others that can operate effectively across third-party apps increasingly look like they will be the correct architectural choice over buying agents from each specific vendor for many use cases. This could cut off an avenue of additional monetization for the SaaS vendors, at least partially. However, agents still need to operate within systems of record to be useful. Otherwise, they lack the business context to perform actions. This may end up being a complementary situation where agents make systems of record better and vice versa. Although this is a period of significant change, we disagree with market consensus that this will make the systems of record less valuable.

Finding Signal in the AI Noise

Altogether, these concerns underscore the scale of disruption embedded in this paradigm shift. With more than 100 public and roughly 15,000 private software companies, many will likely fail to adapt to the speed of the change. The rapid pace and limited visibility into AI’s ultimate impact seem to have led investors to assume the worst. This negative assumption, combined with a near-term “can’t be disproven” dynamic, has made it difficult to estimate the long-term value of many software companies. This dynamic is not surprising given the rapidly shifting paradigm.

As a result of the long-term uncertainty, short-term fundamentals have become less relevant for stock prices. For example, ServiceNow, a leading IT service management vendor, announced fourth-quarter results that included approximately $600 million in annualized contract value for its AI-product. This makes it one of the largest AI revenue streams outside of the LLM providers. Additionally, ServiceNow announced that its new business has accelerated, and renewal rates remain at 98 percent, yet its share price traded lower. When investors lack confidence in what a business may look like five to 10 years from now, it makes very little difference what the business looks like this quarter or even this year. Investor apathy, and in some cases outright skepticism, has also paradoxically raised the bar for earnings performance despite materially lower valuations.

Exhibit 2

SOFTWARE DISRUPTION FEARS HAVE OVERWHELMED NEAR-TERM FUNDAMENTALS

Against this backdrop, we have been working to separate the signal from the noise in software. In select cases, discounted valuations near historical lows present attractive setups where our conviction diverges from prevailing market sentiment. With this context, our positioning reflects a deliberate differentiation across software subcategories based on relative defensibility, opportunity, and risk.

Horizontal software applications face the greatest pressure from AI for all the reasons we have discussed. That said, durability varies meaningfully within the category. Mission-critical systems of record and revenue-linked platforms built on proprietary data remain more defensible than lighter-weight point solutions that are easier to replace.

Vertical software tends to be more resilient as it embeds deep domain expertise and functions as an operating system for customers. For example, Shopify, or its ecosystem of partners, handles nearly every part of selling goods online and offline from payment acceptance to inventory management to cross-channel selling to customer analytics.

Another example is Axon Enterprise, which sells tasers, body cameras, and mission-critical software to law enforcement. Axon’s software and emerging AI capabilities benefit from integration with its body-cam hardware. This source of data cannot be replicated by AI.

In both examples, we believe that selling a comprehensive suite that addresses multiple needs within a relatively less technologically sophisticated organization increases the likelihood that customers will turn to these vendors for AI innovation rather than go elsewhere.

Infrastructure and cybersecurity software remain essential regardless of shifts at the application layer. New AI agents and applications must still be hosted, monitored, and secured, increasing demand for cloud infrastructure, data platforms, databases, and observability tools. Companies operating in these areas function as foundational enablers rather than discretionary layers.

Cybersecurity, in particular, stands out as a potential beneficiary of AI adoption. As AI expands the attack surface and increases the speed and sophistication of threats, demand for security platforms should rise as defense is needed to match a better offense. Vendors with a large installed customer base provide a proprietary, real-time view of threats. Combined with a global network of enforcement points that can block attacks, these vendors are well positioned to help customers manage this growing complexity of security risks.

We have combined these category-level views with bottom-up business insights to evolve our positioning in software. The uncertainty surrounding AI has raised our threshold for conviction, particularly within horizontal software, in which durability is hardest to assess, and competitive outcomes are most difficult to handicap. By contrast, we continue to view vertical, cybersecurity, and infrastructure software as more insulated from AI disruption.

Importantly, none of these businesses are standing still. Like startups, they are moving quickly to embed AI into their platforms. These developments reinforce our belief that established companies with the right data assets, distribution, and engineering culture can not only navigate AI-driven volatility but emerge stronger as this transition unfolds.

Near-term sentiment has tilted toward disruption across the sector. However, we believe the more lasting consequence will be a sharper divide between the companies that can integrate AI purposefully and those that struggle to adapt. Said differently, as with any paradigm shift, there will be companies that gain and lose market share. Thanks to our long-term investment horizon, we believe we are well positioned to benefit from this expected divergence.

1 Source: FactSet as of February 5, 2026.

Disclosures:

The views expressed are the opinion of Sands Capital and are not intended as a forecast, a guarantee of future results, investment recommendations or an offer to buy or sell any securities. The views expressed were current as of the date indicated and are subject to change. This material may contain forward-looking statements, which are subject to uncertainty and contingencies outside of Sands Capital’s control. Readers should not place undue reliance upon these forward-looking statements. All investments are subject to market risk, including the possible loss of principal. Recent tariff announcements may add to this risk, creating additional economic uncertainty and potentially affecting the value of certain investments. Tariffs can impact various sectors differently, leading to changes in market dynamics and investment performance. There is no guarantee that Sands Capital will meet its stated goals. Past performance is not indicative of future results. A company’s fundamentals or earnings growth is no guarantee that its share price will increase. Forward earnings projections are not predictors of stock price or investment performance, and do not represent past performance. There is no guarantee that the forward earnings projections will accurately predict the actual earnings experience of any of the companies involved, and no guarantee that owning securities of companies with relatively high price to earnings ratios will cause a portfolio to outperform its benchmark or index.

As of February 12, 2026, Atlassian, Axon Enterprise, Datadog, Figma, ServiceNow, and Shopify are held across Sands Capital portfolios. Axon and Shopify were chosen on an objective basis to represent the vertical software companies held in our four flagship strategies. Datadog represents infrastructure providers in these strategies. Atlassian, Figma, and ServiceNow, holdings outside of those flagships, were chosen to illustrate the effect AI is having on software companies.

Unless otherwise noted, the companies identified represent a subset of current holdings in Sands Capital portfolios and were selected on an objective basis to illustrate examples of the companies that represent businesses across industries and geographies that use, create, or provide software and services that are deployed across multi-product platforms. They are referenced to showcase how some companies are shifting their software narratives as AI reshapes landscapes.

Any holdings outside of the portfolio that were mentioned are for illustrative purposes only.

The iShares Expanded Tech-Software ETF (IGV) tracks the performance of the U.S. software industry. It is often used as a benchmark for the software segment of the broader tech market.

The iShares Semiconductor ETF (SOXX) tracks the performance of companies that design, manufacture, and distribute semiconductors. It measures some of the largest and most influential U.S.-listed semiconductor companies.

The specific securities identified and described do not represent all the securities purchased, sold, or recommended for advisory clients. There is no assurance that any securities discussed will remain in the portfolio or that securities sold have not been repurchased. You should not assume that any investment is or will be profitable.

GIPS Reports found here.

Sands Capital refers to the combination of Sands Capital Management, LLC, Sands Capital Alternatives, LLC and Sands Capital Horizons, LLC. All three firms are registered investment advisers with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. The three registered investment advisers share certain personnel, office space, and other resources.

This communication is for informational purposes only and does not constitute an offer, invitation, or recommendation to buy, sell, subscribe for, or issue any securities. The material is based on information that we consider correct, and any estimates, opinions, conclusions, or recommendations contained in this communication are reasonably held or made at the time of compilation. However, no warranty is made as to the accuracy or reliability of any estimates, opinions, conclusions, or recommendations. It should not be construed as investment, legal, or tax advice and may not be reproduced or distributed to any person.

Notice for non-US Investors.

© 2026 Sands Capital